Buy a New Car or Keep Your Old One? How to Run the Numbers Before Deciding

Most people compare a repair bill to a monthly payment. That's the wrong comparison. Here's the complete cost analysis that shows you exactly which decision makes financial sense for your specific situation.

Your old car needs a $2,500 repair, and the question feels obvious: why pour $2,500 into an aging car when that's almost half a year of payments on a shiny new one? That instinct, comparing a repair bill to a monthly payment, is exactly the wrong comparison, and it's the reason so many people trade in a perfectly good car and quietly torch thousands of dollars. The right way to decide is to compare the full annual cost of keeping your car against the full annual cost of replacing it. When you do, the answer surprises most people.

A new car isn't just a payment; it's depreciation, higher insurance, taxes, and registration stacked on top. An old car isn't just repairs; it's a paid-off asset with low insurance and zero depreciation left to lose. Put both full pictures side by side and the math usually favors the car sitting in your driveway. Here's how to run it.

The Comparison Almost Everyone Gets Wrong

The trap is comparing one number against another that isn't its equal. A $2,500 repair is a one-time cost. A $500 monthly payment is $6,000 a year, every year, plus everything else a new car drags along. Setting "$2,500 repair" against "$500 payment" feels like a fair fight, but it's comparing a single expense to the tip of a much larger iceberg.

The honest comparison is total annual cost versus total annual cost. What does it cost to own your current car for the next year, repairs and all, versus what it would cost to own a replacement for that same year? Only when both sides include everything, depreciation, insurance, financing, fuel, and repairs, can you actually see which choice is cheaper. Almost always, the repair you were dreading is the bargain.

The Real Cost of Keeping Your Old Car

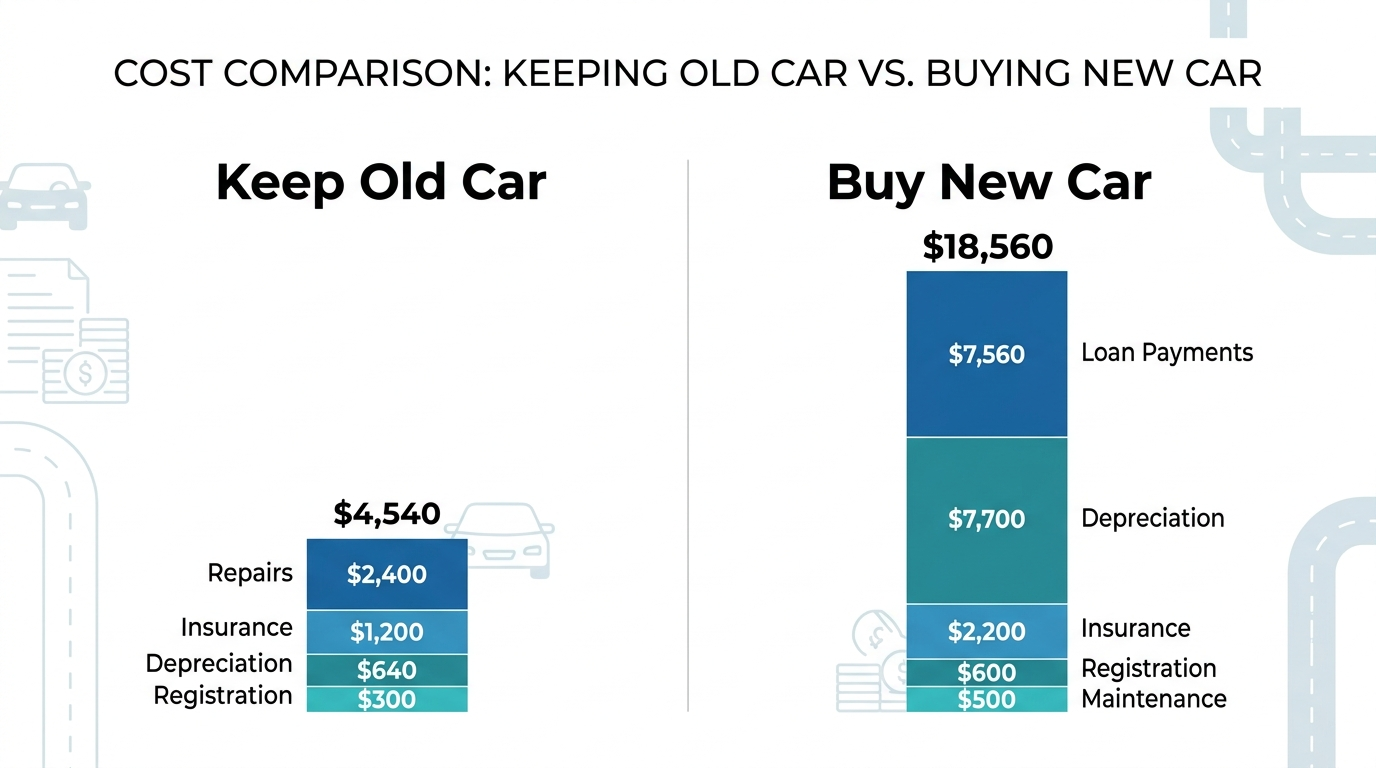

Add up everything your current car costs in a year. For a paid-off vehicle, that's repairs and maintenance, insurance (which is lower on an older car), fuel, and registration. Even an expensive repair year often lands near $6,000 to $8,000 all-in, and most years are far cheaper because not every year brings a major repair.

The key advantage hiding in this number is that a paid-off car has no monthly payment and almost no depreciation left to lose; the steep value drop already happened years ago. A $3,000 repair on a car you own outright is annoying, but it's often cheaper than a single quarter of new-car ownership. Estimate your fuel portion precisely with the fuel cost calculator and the MPG calculator so you're working from real figures, not guesses.

The Real Cost of a New Car

Now the other side, honestly. A new car's first-year cost is far larger than the payment alone, and the biggest piece is invisible on any bill: depreciation.

| Cost | Typical first year |

|---|---|

| Depreciation (20 to 25%) | $7,600 to $9,500 |

| Loan interest | $1,800 to $2,500 |

| Higher insurance | $600 to $1,200 more |

| Taxes & registration | $1,500 to $3,000 |

| First-year total | ~$15,000 to $18,000 |

A new car commonly costs $15,000 to $18,000 in its first year alone, most of it in depreciation you'll never see on a statement. Against a $6,000 to $8,000 year on your paid-off car, even with a big repair, keeping the old one is usually thousands cheaper. Model the financing portion with the auto loan calculator before you fall for the showroom math.

The 50% Rule and When to Replace

Keeping an old car isn't always right, of course. A useful trigger is the 50% rule: if a single repair costs more than half the car's current market value, replacement deserves serious consideration. A $4,000 transmission on a car worth $5,000 is a different decision than the same repair on a car worth $15,000.

Beyond a one-off repair, watch the trend. If repairs are becoming frequent and unpredictable, if the car is no longer safe or reliable enough for your needs, or if it's leaving you stranded, the non-financial costs start to matter alongside the dollars. The point isn't to keep a car forever; it's to replace it on the math and on real need, not on a moment of frustration with a repair quote.

New vs Used: The Sweet Spot

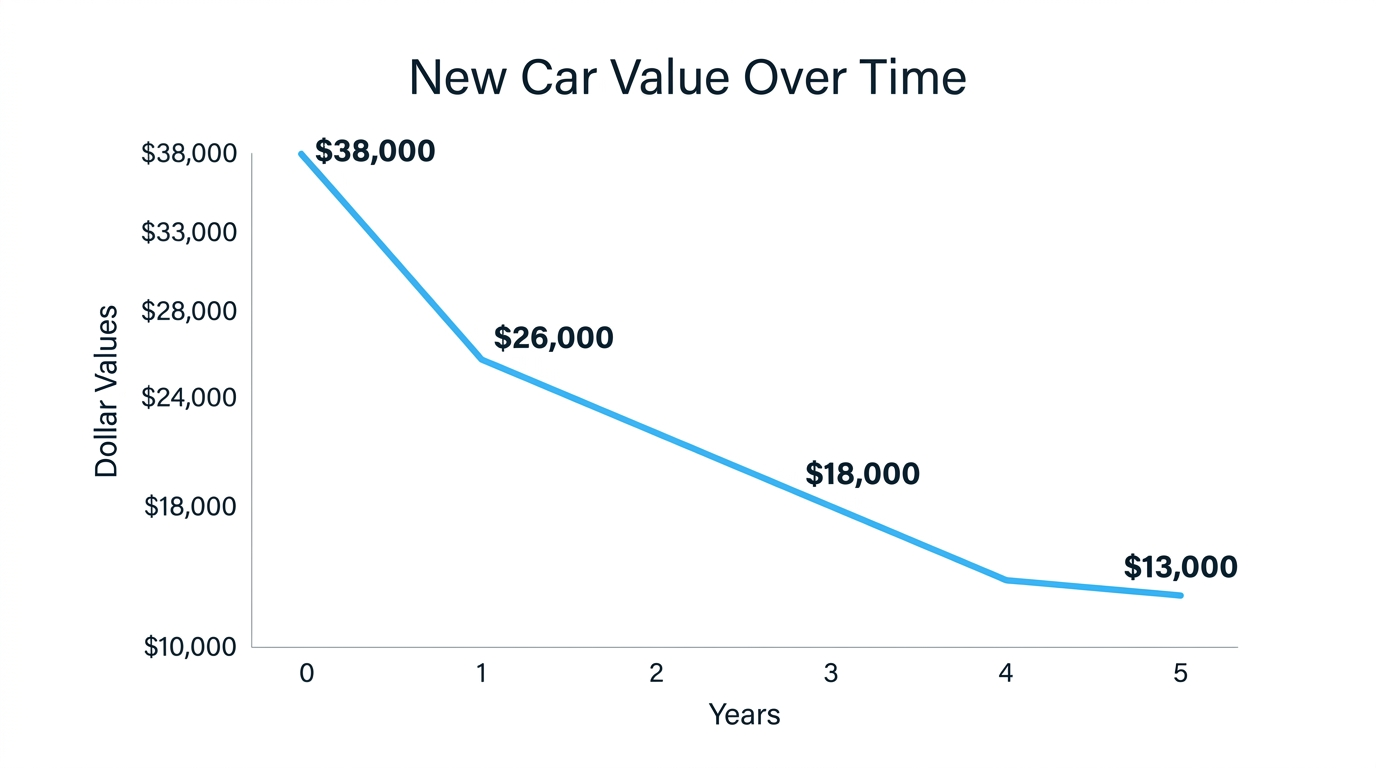

If the numbers do say it's time to replace, the next question is new versus used, and here the math is just as clear. A new car loses 20 to 25% of its value the first year and around 60% within five. Buying new means personally absorbing that steepest part of the depreciation curve.

The value sweet spot is a two-to-four-year-old vehicle with 30,000 to 50,000 miles. Someone else already ate the worst depreciation, modern cars are reliable well past those miles, and you often still get a remaining warranty. A lightly used car gives you most of the benefits of new at a fraction of the depreciation cost, which is why it's the rational default for anyone optimizing for money rather than that new-car smell.

What Reliability and Peace of Mind Are Worth

The math usually favors keeping an old car, but money isn't the only input, and pretending otherwise would be dishonest. A car that strands you on the way to work, fails to start in winter, or can't safely carry your family has real costs that don't show up on a repair invoice: missed work, stress, and risk. Those count too.

The key is to put a realistic number on them rather than letting a single bad morning drive the decision. If your car leaves you stranded twice a year and each incident costs you a day of work plus a tow, that's a genuine annual cost to add to the "keep" side. Often it's still smaller than a new car's depreciation, but sometimes, especially for someone who can't afford any unreliability, it tips the scale. The honest version of this decision includes peace of mind as a line item with an estimated price, not as an unlimited justification for spending $18,000 to avoid a $2,500 repair.

There's also a middle path people forget: a reliable used car. If your current vehicle has genuinely become untrustworthy, you don't have to jump to new. Replacing an unreliable old car with a well-maintained two-to-four-year-old one solves the reliability problem while sidestepping the worst of the depreciation, giving you most of the peace of mind for a fraction of the cost.

Run Your Numbers

The decision comes down to one honest comparison: the full annual cost of keeping your car against the full annual cost of replacing it. Include depreciation on the new side and only count repairs as the real number on the old side, not as a stand-in for a payment. Run it that way and the emotional pull of a new car meets the cold clarity of math.

This is exactly the kind of question the built-in AI assistant on the calculator pages handles well. Tell it something like "my paid-off car needs a $2,500 repair and is worth $7,000, should I fix it or buy a $35,000 new car," and it walks through both annual costs side by side instead of letting a repair quote stampede you into a far more expensive decision. The repair almost always wins. The new car almost always feels like it should.

Frequently Asked Questions

Is it cheaper to keep an old car or buy a new one?

In most cases, keeping your old car is cheaper. A paid-off car with $3,000 in annual repairs typically costs $6,000 to $8,000 per year total. A new car with loan payments, higher insurance, and depreciation commonly costs $15,000 to $18,000 in the first year alone.

At what repair cost should I consider replacing my car?

The 50% rule is a useful starting point: if a single repair costs more than 50% of your car's current market value, replacement is worth serious consideration. However, always run the full annual cost comparison before deciding.

How much does a new car depreciate in the first year?

New cars lose an average of 20 to 25% of their purchase price in the first year of ownership. A $38,000 vehicle loses approximately $7,600 to $9,500 in depreciation in year one alone, before accounting for loan interest or insurance.

What is the true annual cost of owning a new car?

The true first-year cost of a new car includes loan payments, depreciation, increased insurance, registration, and maintenance. On a $35,000 vehicle with typical financing, this commonly totals $15,000 to $18,000 in year one, far more than most buyers anticipate.

Should I buy a new car or a used one?

A 2 to 4 year old certified pre-owned vehicle with 30,000 to 50,000 miles typically offers the best value. It has already absorbed the steepest part of the depreciation curve while still offering modern reliability and often a remaining warranty.