10 Things That Cost Way More Than You Think Over a Lifetime

The true lifetime cost of ten ordinary habits most people never calculate: from daily coffee and unused subscriptions to minimum credit card payments and not negotiating your salary — with the compound math behind each one.

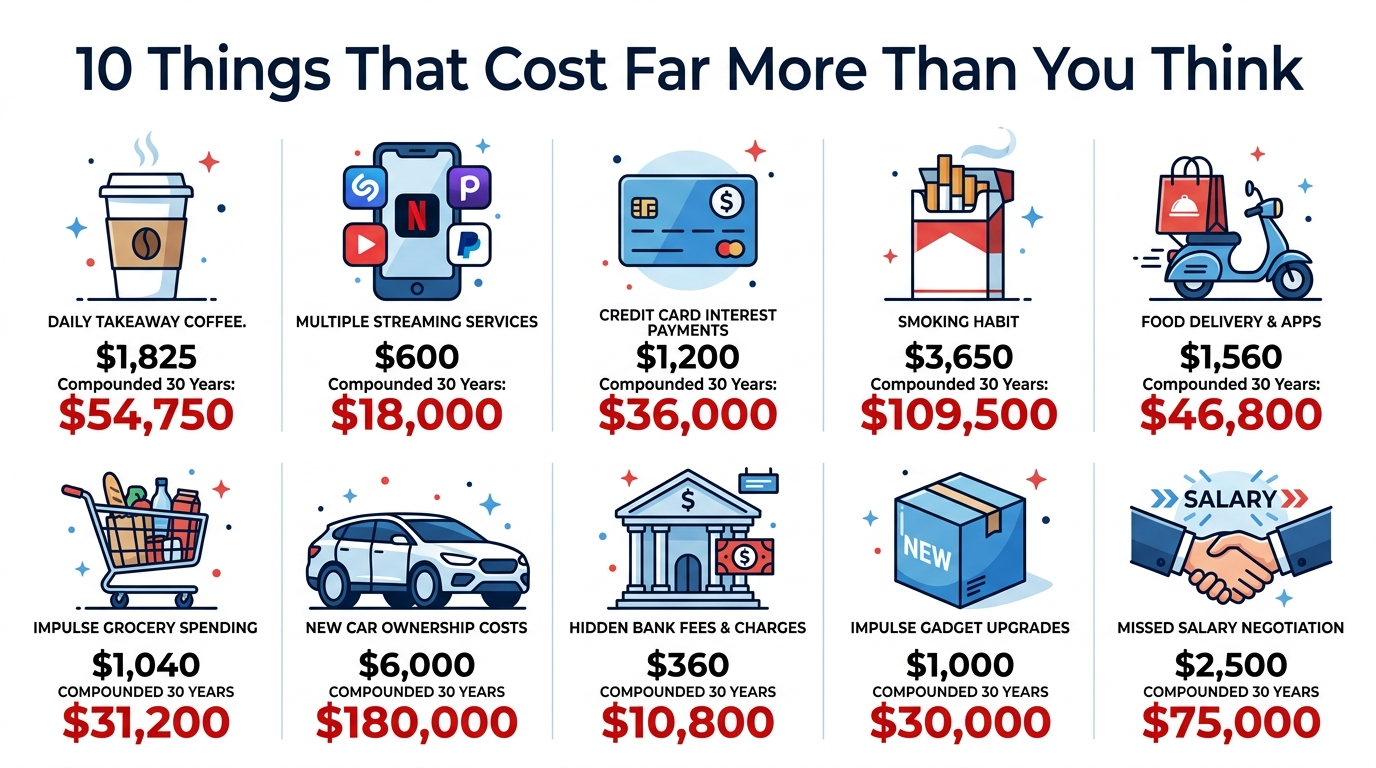

A $6 coffee isn't a $6 decision. Over thirty years, that daily habit doesn't cost you the coffee; it costs you roughly $147,000, because every dollar you spend is a dollar that could have been invested and grown instead. This is the hidden price tag on ordinary life, the gap between what something costs today and what it truly costs once you account for decades of compounding. Ten everyday habits cost far more than you think, and seeing the real numbers changes how a lot of small purchases feel.

This isn't an argument that you should never enjoy anything. It's an argument for seeing the true price so your spending matches what you actually value. Some of these ten are worth every penny to the right person; others are pure leakage almost nobody would defend if they saw the lifetime total. The point is to choose on purpose. Here's the real math.

| Habit | Annual cost | 30-year opportunity cost |

|---|---|---|

| Daily $6 coffee | $1,560 | ~$147,000 |

| Lunches out (3/week) | $2,340 | ~$221,000 |

| Unused subscriptions | $2,400 | ~$227,000 |

| Food delivery fees & markup | $2,000 | ~$189,000 |

| Smoking (pack/day) | $2,920 | ~$276,000 |

| Bank & ATM fees | $360 | ~$34,000 |

| Credit card minimum payments | Varies | More than the debt itself |

| New car every few years | $8,000+ | $500,000+ |

| Lottery & impulse buys | $1,000 | ~$94,000 |

| Not negotiating your salary | $5,000 base gap | $400,000 to $900,000 |

Why Small Numbers Slip Past Your Brain

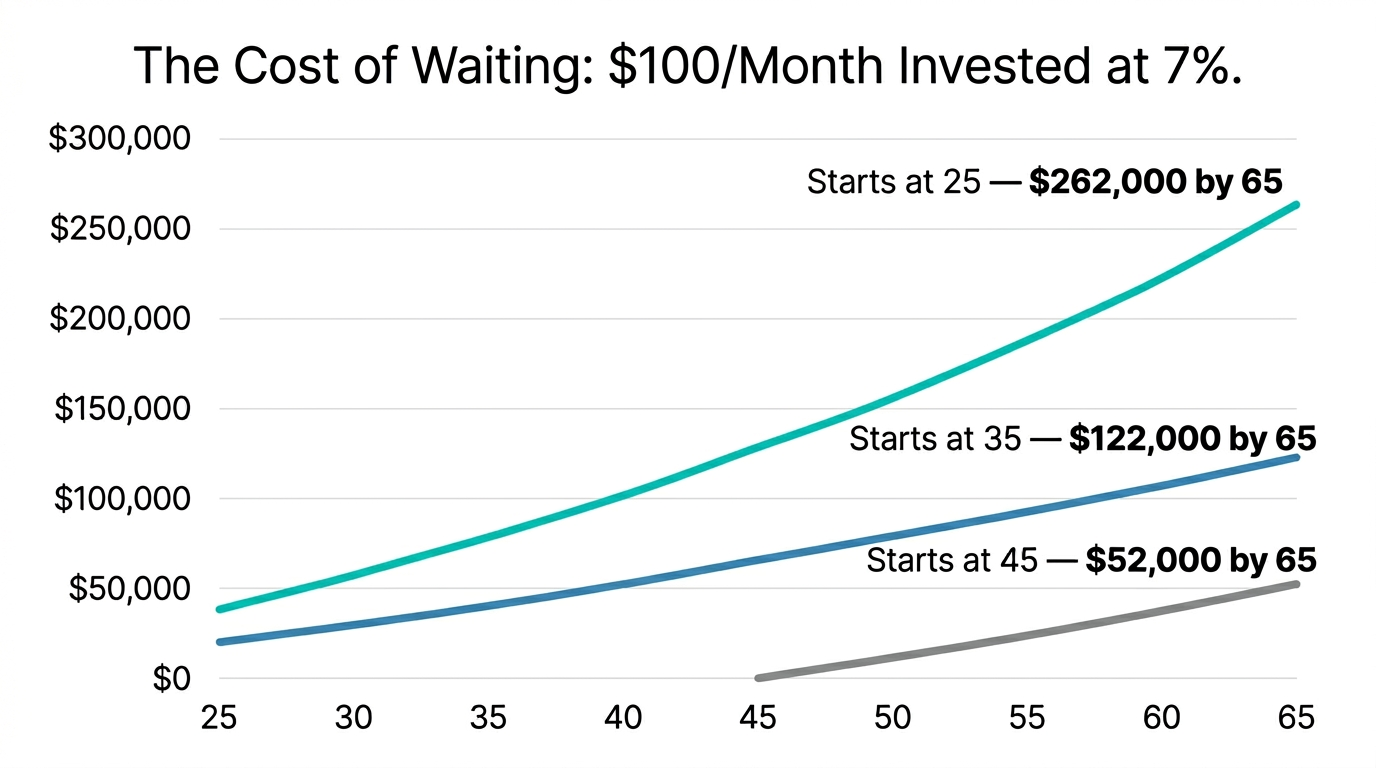

Before the individual habits, it's worth understanding why these costs hide so well, because the psychology is the whole reason they accumulate. Your brain evaluates a $6 coffee as a $6 decision. It is almost incapable of intuitively feeling the $147,000 version, because that number lives thirty years in the future and requires compounding math your gut never does.

This is called present bias: we weigh immediate, concrete rewards far more heavily than distant, abstract ones. The coffee is warm and real right now; the retirement it could fund is a fuzzy someday. Multiply that bias across dozens of small daily choices and the leak becomes a flood you never consciously approved. The purchases feel free because each one is trivially small, and trivially small is exactly the size that evades scrutiny.

Seeing the lifetime numbers is the antidote, because it forces the future cost into the present where your brain can actually weigh it. Once you've genuinely registered that a habit costs a six-figure sum, the next purchase feels different, not forbidden, just visible. That visibility is the entire point of running the math, and it's why a single honest calculation can change behavior that years of vague guilt never touched.

The Daily Drips That Become Floods

The first cluster is the small, frequent purchases that feel harmless precisely because each one is tiny. The daily coffee, the lunches out, the food delivery: none of them feels like a financial decision in the moment, which is exactly why they add up so quietly.

The mechanism is opportunity cost. A dollar spent is a dollar that can't compound, and at a 7% return money roughly doubles every decade. So a $1,560-a-year coffee habit isn't competing with $1,560; it's competing with the roughly $147,000 that money would become over thirty years. Add three lunches a week and some delivery, and the daily drips alone can cost a third of a million dollars over a career. See the effect on your own numbers with the compound interest calculator or estimate a coffee habit directly with the coffee calculator.

The Subscriptions and Fees You Forgot About

The second cluster is money leaving your account that you've stopped noticing entirely. A 2022 study found Americans spend over $200 a month on subscriptions on average and can't name half of them. That's $2,400 a year, often for services barely used, which compounds to roughly $227,000 over twenty years of opportunity cost.

Bank and ATM fees belong here too. They feel trivial at $3 or $35 a pop, but a few hundred dollars a year of avoidable fees still compounds into tens of thousands over a working life, and unlike coffee, you get absolutely nothing for them. These are the easiest wins on the entire list: a one-evening audit of your statements to cancel forgotten subscriptions and switch to a no-fee bank can recover thousands a year for zero sacrifice in quality of life.

The Big-Ticket Habits

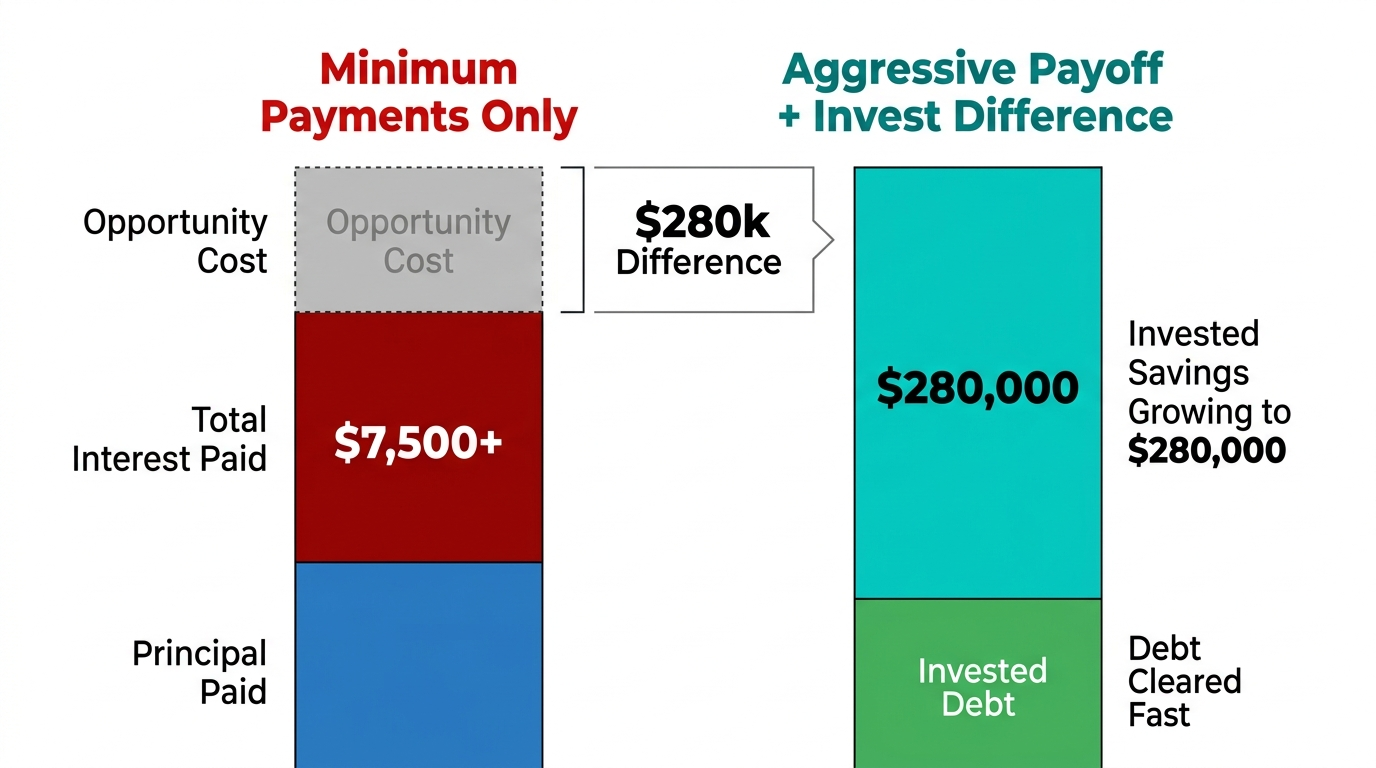

The third cluster does the most damage of all, because the dollar amounts are large and the habits repeat for decades. Buying a new car every few years means perpetually absorbing the steepest depreciation; over a lifetime, that cycle versus buying lightly used and keeping cars longer can cost more than $500,000 in opportunity cost. Paying only the minimum on credit card debt can cost more in interest than the original balance, turning a $5,000 purchase into far more.

The single most expensive item on the list isn't spending at all; it's a missed gain. Failing to negotiate a starting salary doesn't just cost the first year's difference. A $5,000 lower starting salary becomes the base every future raise, bonus, and 401(k) match builds on, which over a 35-year career commonly translates to $400,000 to $900,000 in lost lifetime earnings. The lesson is that the biggest numbers come from decisions you make rarely, so those are the ones worth slowing down for. Smoking sits here too, costing nearly $3,000 a year and far more in health, compounding to roughly $276,000.

How to Use This Without Becoming Miserable

Seeing these numbers can tip into guilt, which isn't the goal and doesn't last. The smarter response is selective, not total. Pick the two or three items on this list you genuinely don't value, and cut those ruthlessly. Keep the ones that bring you real joy, guilt-free, because money is meant to be used as well as grown.

The highest-leverage moves are usually the big, rare decisions, negotiating salary, buying used and keeping cars, killing high-interest debt, not the daily latte that actually makes your morning better. This is a great thing to explore with the built-in AI assistant on the calculator pages: tell it your habits and ask "which of these is costing me the most over time and what should I cut first," and it ranks them by lifetime impact so you fix the leaks that matter. Knowing the real price of a habit doesn't mean you have to give it up. It means you finally get to decide with your eyes open. Run a few of your own habits through the investment calculator and see which ones are quietly worth a fortune.

Frequently Asked Questions

What everyday expenses cost the most over a lifetime?

The highest lifetime costs come from habits compounded over decades: food delivery and eating out ($5,000 to $8,000 per year), car ownership ($10,700 per year on average including depreciation), smoking ($2,920 or more per year), unused subscriptions ($1,200 to $2,400 per year), and paying only the minimum on credit card debt, which can cost more in interest than the original balance.

How much does a daily coffee habit actually cost over 30 years?

A $6 weekday coffee habit costs approximately $1,560 per year. Invested at a 7% annual return over 30 years, that same money grows to roughly $147,000. Add three lunches out per week at $15 each and the combined annual cost is $3,900, which compounds to approximately $369,000 over 30 years.

What is opportunity cost in personal finance?

Opportunity cost is the value of what you give up when you choose one option over another. In personal finance, every dollar spent is a dollar not invested. A dollar invested at 7% annually doubles roughly every 10 years. Opportunity cost makes the true price of a habit much higher than its sticker price when calculated over a full investment horizon.

How much money do people waste on subscriptions they do not use?

A 2022 Consumer Intelligence Research Partners study found Americans spend over $200 per month on subscription services on average and can name fewer than half of them when asked. At $200 per month, unused subscriptions cost $2,400 per year — over $114,000 in compounded opportunity cost over 20 years at 7% return.

Does inflation make everyday habits more expensive over time?

Yes. At 3% annual inflation, a $6 purchase today costs approximately $9.70 in 15 years and $14.40 in 30 years. Inflation also erodes money that is not invested: $100,000 sitting in a checking account for 20 years has the purchasing power of roughly $55,000 in today's dollars. Both processes run simultaneously and invisibly.

What is the single biggest financial mistake most people make?

Not negotiating their starting salary. A $5,000 starting salary gap does not just cost $5,000 in year one. Every raise, bonus, and employer 401(k) match builds on that base. Over a 35-year career with 3% annual raises, a $5,000 lower starting salary typically translates to $400,000 to $900,000 less in lifetime earnings.