Rent vs Buy: The Honest Math That Real Estate Agents Don't Show You

The "renting is throwing money away" argument ignores a lot of math. We break down opportunity cost, maintenance, taxes, and appreciation so you can make the decision that's right for you.

"Renting is throwing money away." You've heard it from parents, real estate agents, and every uncle at every family dinner. It's also one of the most expensive half-truths in personal finance, because it leaves out everything that makes owning expensive and everything that makes renting flexible. The honest rent vs buy math is not a slogan; it's a calculation, and when you actually run it, the answer is far less obvious than the people selling houses want you to believe. Here is the math they skip.

None of this is an argument against buying. Owning a home is one of the best wealth-building tools most people ever access. The point is narrower and more useful: the decision depends on real numbers specific to your situation, not on a saying. Once you can see all the costs on both sides, you can make the call that's right for you instead of the one that sounds right.

The Sentence That Starts Every Bad Decision

The "throwing money away" line treats rent as pure loss and every mortgage dollar as savings. Both halves are wrong. Rent buys you something real: a place to live, freedom from maintenance, and the ability to leave whenever you want. That flexibility has genuine value, especially early in a career when your job and your city might change.

On the other side, a large chunk of every early mortgage payment is not savings at all. It's interest, and interest is money you never get back, exactly like rent. In the first years of a 30-year loan, the majority of each payment goes to interest, not principal. Add property tax, insurance, and maintenance, none of which builds a cent of equity, and the picture of "owning equals saving, renting equals waste" falls apart. Both options have a cost of living somewhere. The question is which one costs you less, all in.

The One Ratio That Settles Most of It

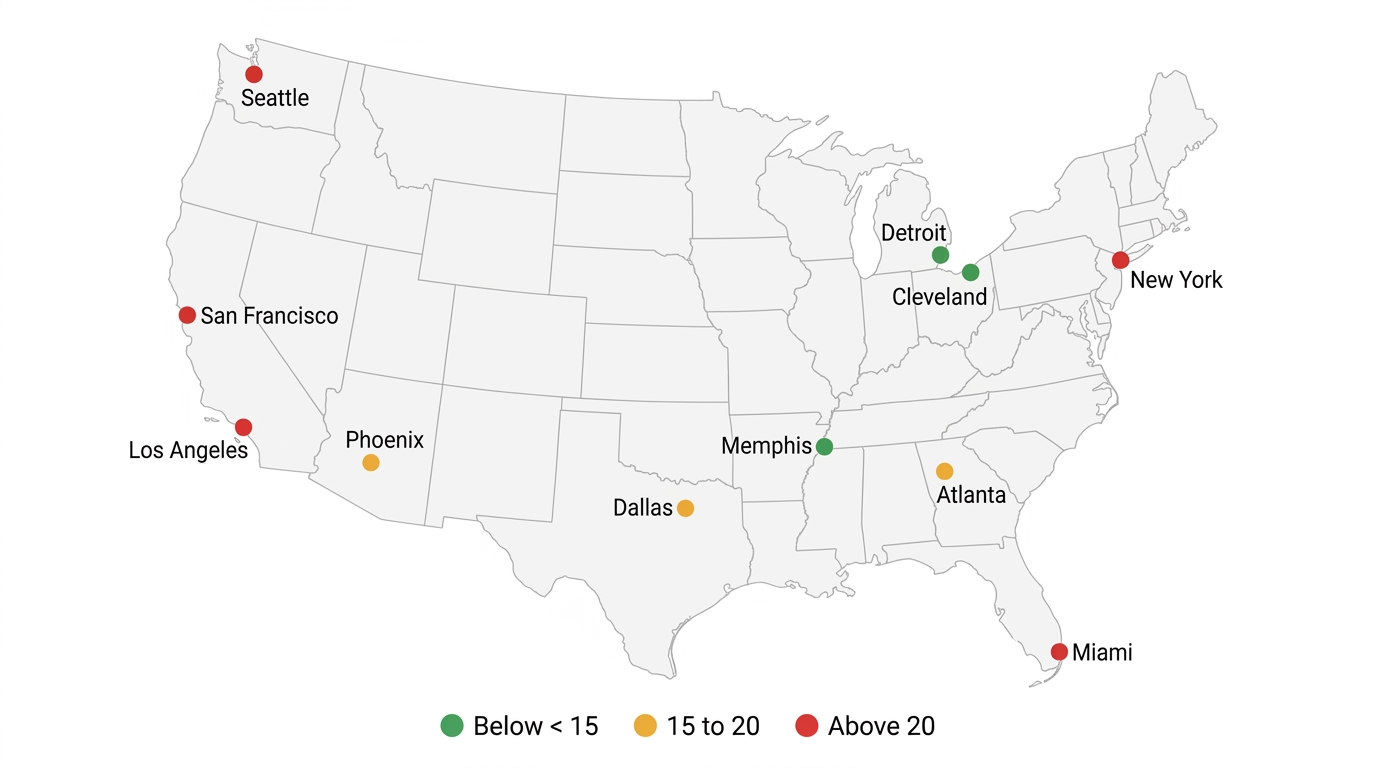

Before any detailed math, one number tells you which way your local market leans: the price-to-rent ratio. Take the price of a home and divide it by the annual rent for a comparable place. A $400,000 home versus a similar rental at $2,000 a month ($24,000 a year) gives a ratio of about 16.7.

| Ratio | What it signals | Leans toward |

|---|---|---|

| Below 15 | Homes are cheap relative to rents | Buying |

| 15 to 20 | Roughly balanced | Either, run the numbers |

| Above 21 | Homes are expensive relative to rents | Renting |

A ratio below 15 means buying is relatively cheap and tends to win. Above 21, prices are steep compared to what you'd pay to rent the same place, and renting while investing the difference often comes out ahead. Most of the expensive coastal cities sit well above 21, which is exactly why "just buy" is bad blanket advice there. Check your own market with the rent vs buy calculator before you assume buying is automatically smarter.

The Costs Nobody Puts in the Comparison

The reason the slogan misleads is that it compares rent to a mortgage payment alone, ignoring the entire second layer of ownership costs. To compare honestly, you have to count everything.

On the buying side, the costs that build no equity include mortgage interest, property taxes (often around 1 to 1.5% of value a year), homeowners insurance, and maintenance (budget roughly 1% of the home's value annually). Then there are the transaction costs that quietly eat returns: 2 to 5% to buy, and a brutal 5 to 6% in agent commissions and fees to sell. Those one-time hits are why owning rarely pays off over a short horizon.

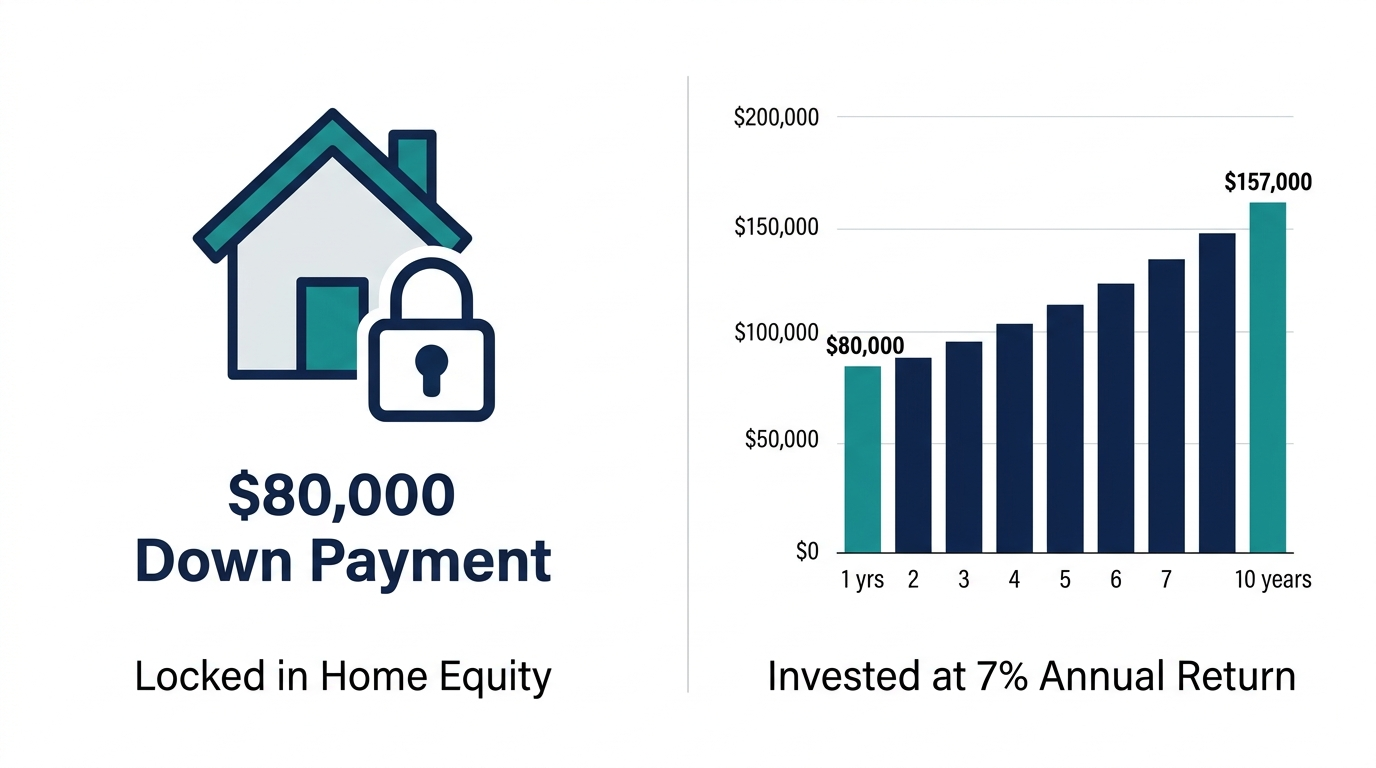

On the renting side, the true cost is mostly just the rent and a small renter's insurance premium. But there's a hidden factor in the renter's favor that almost no one counts: the down payment a buyer ties up in the house is money a renter can invest instead. A $80,000 down payment invested at 7% becomes about $112,000 in five years. That foregone investment growth is a real cost of buying, and leaving it out is the single biggest cheat in the standard comparison.

A Five-Year Head-to-Head

Put it together with one realistic scenario: a $400,000 home with 20% down at a 6.5% mortgage, versus renting a comparable place for $2,000 a month, both over five years, assuming 3% annual home appreciation and a 7% return on invested money. Here's the honest accounting of money that does not come back.

| Over 5 years | Buy ($400k) | Rent ($2,000/mo) |

|---|---|---|

| Money spent that doesn't return | ~$187,900 | ~$128,400 |

| Offset (appreciation or investing) | −$63,700 | −$32,200 |

| Net 5-year cost | ~$124,200 | ~$96,200 |

In this scenario, renting comes out roughly $28,000 cheaper over five years, mostly because of those transaction costs and the investment growth on the down payment. That result surprises people, and it should: it's the exact math the slogan hides. Change the inputs, though, and the answer flips, which is the whole point.

The Break-Even Point Is Personal

The single biggest lever is time. Transaction costs are front-loaded, so the longer you stay, the more years you have to spread them over and the more appreciation and principal paydown work in your favor. Most buy-versus-rent breakevens land somewhere between five and seven years, but yours depends on your price-to-rent ratio, your interest rate, local appreciation, and how the rental market moves.

Buying tends to win when you'll stay put for many years, the price-to-rent ratio is low, and your income is stable. Renting tends to win when you might move within a few years, the ratio is high, or you'd rather invest the down payment than lock it into a single illiquid asset. Run your own timeline through the rent vs buy calculator and size the loan itself with the mortgage calculator to find the year your own breakeven actually arrives.

The Tax Break Isn't the Reason You Think

One argument for buying deserves special scrutiny because it's repeated so often: "you get to write off the mortgage interest." For most buyers today, that benefit is far smaller than they imagine, and sometimes nonexistent.

The mortgage interest deduction only helps if you itemize your taxes, and since the standard deduction roughly doubled in 2017, the large majority of households take the standard deduction and itemize nothing. If your total itemizable expenses don't exceed the standard deduction, the mortgage interest "write-off" saves you exactly zero dollars, because you'd have gotten the standard deduction anyway. Even for those who do itemize, the deduction only returns your marginal tax rate on the interest, not the interest itself. Paying a bank $10,000 in interest to get $2,200 back from the government is not a winning trade on its own.

Never buy a home for the tax break. Buy it because the full math works and because you want to live there. Treat any tax benefit as a small bonus you verify with your own return, not as a pillar of the decision. The slogan oversells it precisely because it sounds clever, and clever-sounding is not the same as true.

The Question Beneath the Question

Even a perfect spreadsheet can't decide this alone, because the choice is part financial and part personal. A home you'll raise a family in for twenty years is not just an investment, and the math should bend to your life rather than the other way around. Flexibility, stability, and peace of mind all carry real weight.

What the math does is strip away the false certainty of the slogan so you're choosing with open eyes. Before committing, make sure the payment itself is comfortable, not just approved, using the house affordability calculator, and check how your down payment size changes the deal with the down payment calculator. A home you can comfortably afford and plan to keep is usually a good decision regardless of what the ratio says.

Run Your Own Numbers

The honest answer to "should I rent or buy" is "it depends, and here's exactly on what." Your time horizon, your local price-to-rent ratio, your mortgage rate, and what you'd do with the down payment if you didn't buy. Plug those into the calculators above and the decision stops being a debate and becomes a number.

This is also where the built-in AI assistant on the calculator pages helps. After you enter your figures, you can ask it something specific like "I plan to stay four years, homes here have a price-to-rent ratio of 24, should I rent or buy," and it reasons through your time horizon and market instead of handing you a generic answer. The slogan says one thing for everyone. Your numbers say the truth for you, and the truth is worth more than the saying.

Frequently Asked Questions

Is it better to rent or buy a home?

Neither is universally better. Buying makes financial sense when you plan to stay 5 or more years, the price-to-rent ratio is below 20, and you have stable income. Renting is better when you value flexibility, plan to move soon, or local home prices are very high relative to rents.

What is the price-to-rent ratio?

The price-to-rent ratio is the home price divided by the annual rent for a comparable property. A ratio below 15 favors buying. A ratio of 15–20 is neutral. Above 20 generally favors renting, as purchase prices are high relative to what you would pay in rent.

How long do you need to stay in a home to make buying worth it?

The break-even period is typically 4–7 years, depending on transaction costs, local appreciation rates, and rent levels. Use a rent vs buy calculator with your specific numbers to find your personal break-even point.

Is renting really throwing money away?

No. Rent buys you housing, flexibility, and freedom from maintenance costs and market risk. Homeowners also spend money on mortgage interest, property taxes, insurance, HOA fees, and maintenance — none of which builds equity.

What hidden costs do first-time buyers often miss?

Property taxes, homeowners insurance, HOA fees, maintenance (typically 1–2% of home value per year), closing costs (2–5% of purchase price), and the opportunity cost of the down payment that could have been invested instead.