8 Things That Destroy Your Credit Score And How to Calculate the Damage

A single 30-day late payment can drop a 780 score by 100 points. High utilization, closed old accounts, hard inquiries, and collections each take their own toll. Here's exactly what each costs and how long the damage lasts.

A single mistake can erase years of careful credit building in one billing cycle. The things that destroy your credit score are rarely dramatic; they're small, ordinary slips that the scoring models punish far more harshly than most people expect. A forgotten payment, a maxed-out card, one badly timed account closure, and a score in the high 700s can fall into the 600s before you've noticed. Here are the eight that do the most damage, exactly how many points each one costs, and how long the harm lasts.

Two facts make this worth understanding. First, the higher your score, the more points you lose from a single misstep, because the model treats good-credit behavior as the baseline and reacts sharply to a break in it. Second, recovery times vary enormously, from a single billing cycle to a full decade. Knowing the difference tells you which mistakes to guard against hardest. Start with the overview, then we'll take each one apart.

| Mistake | Typical points lost | How long it lingers |

|---|---|---|

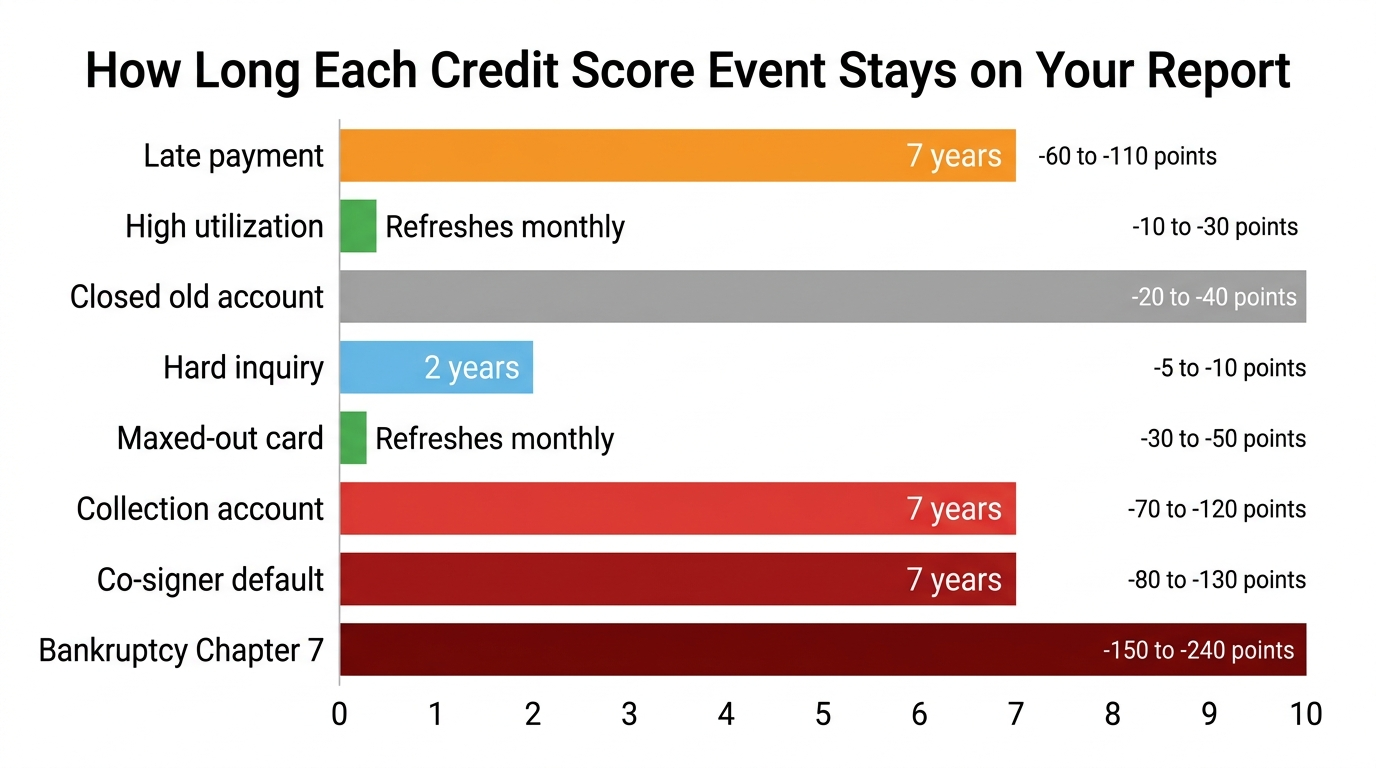

| 1. A 30-day late payment | 60 to 110 | 7 years on report |

| 2. High utilization | 10 to 50 | Recovers in 1 to 2 cycles |

| 3. Closing an old card | 10 to 30 | Months to years |

| 4. A hard inquiry | 5 to 10 | 12 months of impact |

| 5. Maxing out one card | 10 to 45 | Recovers when paid down |

| 6. Collections or charge-off | 100+ | 7 years |

| 7. Co-signing a loan gone bad | Varies, often 60+ | Follows the loan |

| 8. Bankruptcy | 130 to 240 | 7 to 10 years |

How Your Credit Score Is Actually Built

Before the eight mistakes make sense, you need to know what they're damaging. A FICO score, the model most lenders use, is built from five weighted factors. The size of each weight tells you exactly why some mistakes cost so much more than others.

- Payment history (35%): whether you pay on time. The single largest factor, which is why one late payment hits so hard.

- Credit utilization (30%): how much of your available credit you're using. The second largest, and the fastest to move in either direction.

- Length of credit history (15%): the average age of your accounts. This is why closing an old card stings.

- New credit (10%): recent applications and hard inquiries.

- Credit mix (10%): the variety of credit types you manage, such as cards, auto loans, and a mortgage.

Notice that payment history and utilization together make up 65% of the entire score. Almost everything that destroys credit fast traces back to one of those two. Keep them both healthy and the remaining 35% mostly takes care of itself over time. With that map in hand, here's each of the eight credit killers in order of how much damage it does.

1. A Single Late Payment

Payment history is 35% of your FICO score, the largest single factor, which makes a missed payment the most damaging common mistake there is. A payment reported 30 days late can knock 60 to 110 points off a score in the high 700s in one update.

The cruel part is the asymmetry: the better your credit, the more you lose, because the model reads the first delinquency from a strong file as a serious anomaly. The damage fades over two years and falls off entirely after seven, but the immediate hit is steep. Automate at least the minimum payment on every account so a busy month never becomes a credit event.

It's worth knowing how the timeline of lateness escalates. A payment isn't usually reported to the bureaus until it's 30 days past due, so a payment you're a few days late on, then catch up, typically never shows. But once you cross 30 days, the damage is done, and it deepens at 60 and 90 days. This is also not limited to credit cards: auto loans, mortgages, student loans, and even some utility and phone accounts can report late payments. One automated safety net across every account is the cheapest insurance in personal finance.

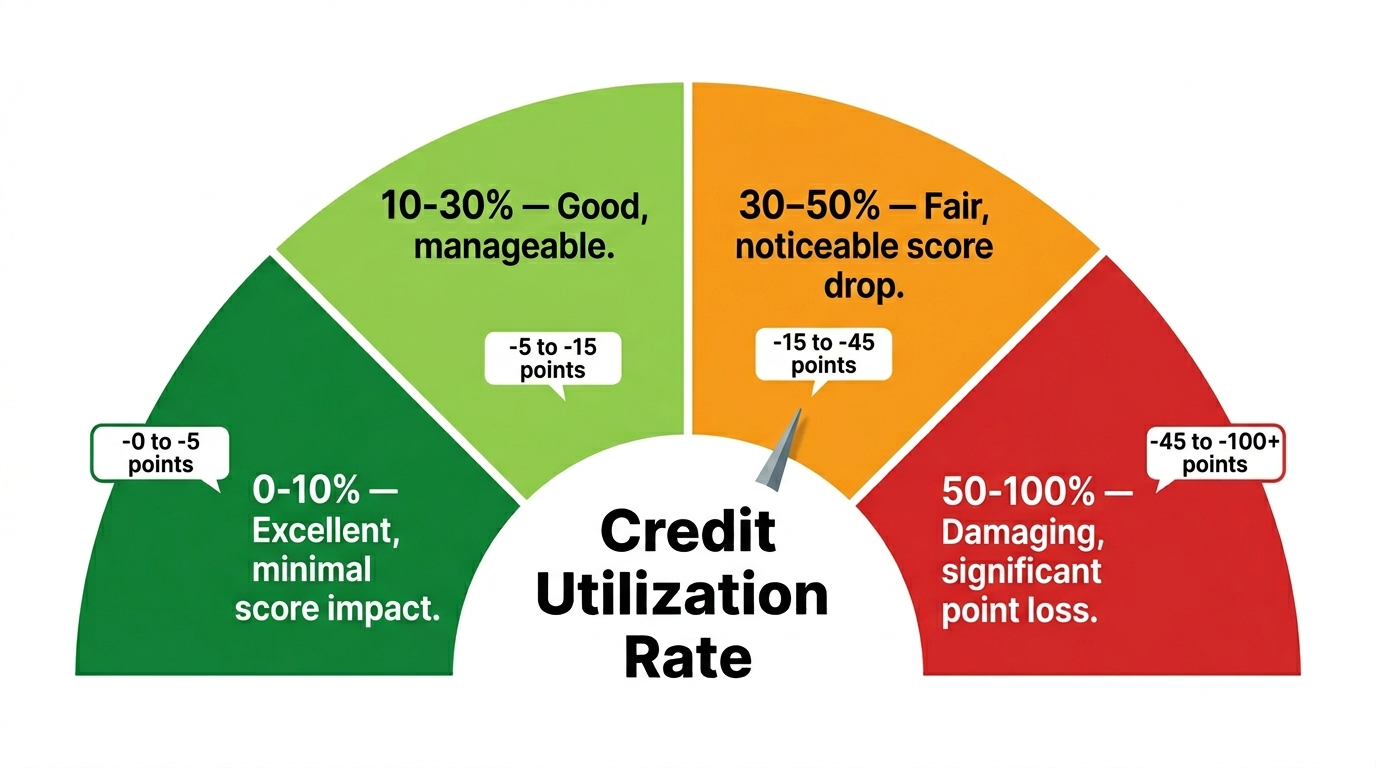

2. High Credit Utilization

Utilization, the share of your available credit you're using, is 30% of your score and the second most powerful factor. Cross 30% and the damage begins; above 50% it becomes significant. Someone carrying $9,000 on a $10,000 limit is signaling risk with every statement.

The good news is that utilization has no memory. Pay the balance down and your score reflects the improvement within one or two billing cycles, with no lasting scar. People with the highest scores typically keep utilization under 10%, both overall and on each individual card. If your balances are high, mapping them on the credit card payoff calculator shows how fast a focused payoff drops your ratio back into safe territory.

There's a timing trick most people miss. The balance reported to the bureaus is usually your statement balance, not the balance after your due date. So even if you pay in full every month, a high statement balance can still report high utilization. Paying down the card a few days before the statement closing date, rather than waiting for the due date, means a lower number gets reported in the first place. For anyone trying to maximize a score before a mortgage application, this single habit can add meaningful points without paying a cent more.

3. Closing an Old Credit Card

Closing a card feels responsible. It often hurts your score for two separate reasons. First, it erases that card's limit from your total available credit, which instantly raises your utilization even though your spending didn't change. Second, it eventually lowers the average age of your accounts, and length of credit history is 15% of your score.

The older the card, the more its closure costs you, because you're removing your longest-standing positive history. Unless a card charges an annual fee you can't justify, keep it open. A single small recurring charge paid in full each month keeps it active without risk.

There is one case where closing makes sense: a card with a steep annual fee you no longer get value from. Even then, you have a better option than closing. Ask the issuer for a "product change" or downgrade to a no-fee version of the same card. This keeps the account, and its valuable age, on your report while eliminating the fee. You lose none of the credit history and pay nothing to keep it. Closing should be the last resort, not the default reflex it is for most people.

4. Too Many Hard Inquiries

Every time you apply for new credit, the lender runs a hard inquiry, costing roughly 5 to 10 points. One is minor. Several in a short window compound, and to a lender they signal someone scrambling for credit, which reads as risk.

There's an important exception. When you're shopping for a single mortgage, auto loan, or student loan, multiple inquiries of the same type within a 14 to 45 day window are counted as one. So rate-shopping for one car loan won't stack up against you, but applying for three credit cards in a month will. Space out genuine new-credit applications and only apply when you actually need to.

You can also avoid most inquiry damage by using prequalification. Many lenders let you check whether you're likely to be approved using a soft pull that doesn't touch your score, so you only submit a real application, and trigger the hard inquiry, when approval is likely. Checking your own score, getting prequalified offers, and being added as an authorized user on someone else's card are all soft pulls. The hard inquiry only happens at the moment of a genuine application, which is the moment to be deliberate about.

5. Maxing Out a Single Card

Even if your overall utilization looks fine, maxing out one individual card hurts you. The scoring models look at per-card utilization as well as the total, so a single card pushed to its limit drags your score even while your other cards sit empty.

This catches people who funnel everything onto one rewards card. The fix is to spread balances or, better, pay the card down before the statement closes, since the balance reported to the bureaus is usually the statement balance, not what's left after the due date. Paying a few days early can lower the number that actually gets reported.

A second fix works in the opposite direction: raise the limit instead of lowering the balance. Requesting a credit limit increase on a card you handle well increases your available credit, which lowers your utilization ratio even if your spending stays the same. Many issuers grant these with only a soft pull if you ask. The catch is discipline: a higher limit only helps your score if you don't treat it as permission to spend more. Used carefully, it's a free way to improve the second-biggest factor in your score overnight.

6. Letting Debt Reach Collections or Charge-Off

When an account goes unpaid for around 120 to 180 days, the lender charges it off and often sells it to a collections agency. Both events are severe, capable of removing 100 points or more, and both stay on your report for seven years.

This is the outcome the earlier mistakes lead to if left unaddressed, which is why catching problems early matters so much. If you're heading toward this, contact the creditor before the charge-off; many will accept a payment plan or settlement that's far less damaging than a collection. Checking your overall load on the debt-to-income ratio calculator helps you see trouble forming before it becomes a charge-off.

If a debt has already reached collections, you still have leverage. Before paying, ask the collector to validate the debt in writing, since agencies sometimes cannot prove they own it. When you do settle, get the agreement in writing first, and ask whether they'll report the account as paid in full rather than settled. A paid collection is viewed more favorably than an unpaid one, and recent versions of the FICO model ignore paid collections entirely. Never make a partial payment on an old collection without understanding that it can restart the clock on how long the debt is legally collectible in some states.

7. Co-Signing a Loan That Goes Wrong

Co-signing makes you fully responsible for someone else's debt, and their late payments become your late payments on your credit report. People co-sign for family with the best intentions and discover that a missed payment they never made just cost them 60 points or more.

The loan also counts toward your own debt-to-income ratio, which can block your next mortgage or car loan even when the borrower is paying on time. Only co-sign if you can comfortably cover the full payment yourself, and monitor the account, because its health is now tied to yours.

Getting off a co-signed loan later is harder than people expect. The main exits are a refinance into the primary borrower's name alone, a cosigner-release option if the loan offers one after a streak of on-time payments, or simply paying the loan off. Until one of those happens, the debt sits on your report and counts against you for every future application. Treat co-signing as taking on the loan yourself, because in every way that matters to your credit, you have.

8. Bankruptcy

Bankruptcy is the most severe entry a credit report can carry. It can cost 130 to 240 points and stays on file for 7 to 10 years depending on the chapter. It is sometimes the right financial decision, but it is never a small one for your score.

The silver lining is that the damage fades faster than the timeline suggests. With disciplined behavior, secured cards, perfect payment history, and low utilization, many people climb back into the good range within a few years even while the bankruptcy still shows. The report entry lingers; its weight diminishes as fresh positive history piles up on top of it.

The two common types differ in how long they stay. Chapter 7, which discharges most debts, remains on your report for 10 years. Chapter 13, which restructures debt into a repayment plan, falls off after 7. Neither is a decision to make casually, and both should be weighed with a qualified advisor against every alternative first. But if bankruptcy has already happened, treat the date it was filed as the starting line of your rebuild, not a permanent verdict. The score recovers on the strength of what you do afterward.

How to Check Your Score Without Hurting It

A surprising number of people avoid looking at their own credit out of fear that checking it will lower the score. That fear is based on a misunderstanding worth clearing up, because monitoring your credit is one of the best defenses you have.

When you check your own credit, it's a soft inquiry, and soft inquiries never affect your score. Only hard inquiries, the kind a lender runs when you apply for credit, cost points. That means you can check as often as you like with zero risk. Federal law entitles you to free reports from each of the three major bureaus through the official annual report service, and most card issuers and banks now show your score for free inside their apps.

Reviewing your report regularly does two valuable things. It catches errors, and errors are common: a payment marked late that you made on time, an account that isn't yours, a balance that's already been paid. Disputing and removing a single erroneous late payment can lift a score by dozens of points. It also catches identity theft early, when a fraudulent account or inquiry first appears, before it can do real damage. Checking your credit is not a risk to manage; it's a habit that protects the score you're working to build.

How to Rebuild and Protect Your Score

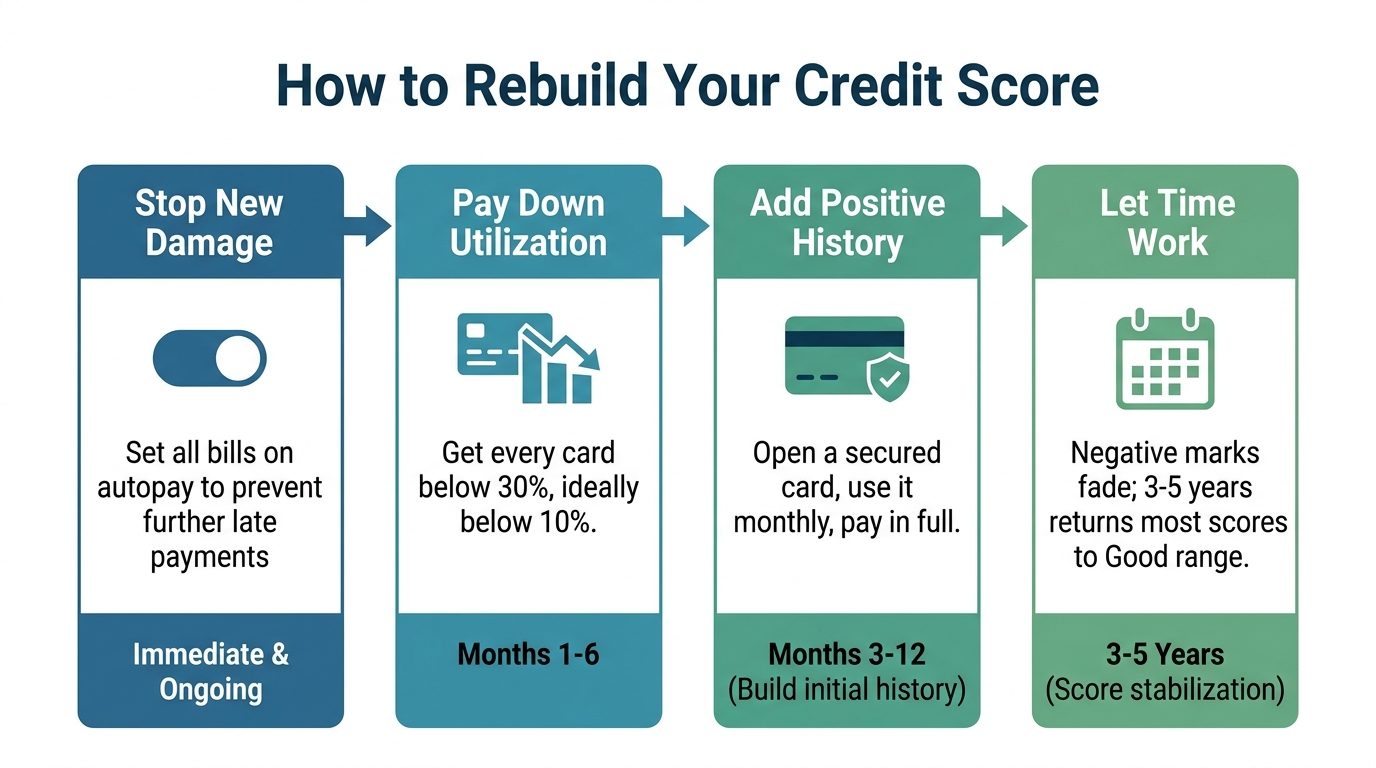

The pattern across all eight is clear: payment history and utilization drive most of the movement, and the worst damage comes from letting small problems become permanent records. Protecting your score is mostly about never missing a payment and keeping balances low, then giving time and consistency room to work.

This is also where the built-in AI assistant on the calculator pages helps you act rather than worry. After you check your balances and ratios, you can ask it something specific like "my utilization is 60% and I want to get under 10%, how much do I pay and how fast will my score recover," and it frames the payoff and the realistic timeline instead of leaving you guessing. Recovery is rarely as slow as it feels in the moment. Stop the bleeding, keep your oldest accounts open, pay on time without exception, and the number climbs back faster than it fell.

If your score has been badly damaged and you're starting from a low base, there's a reliable rebuilding order. Open a secured card, where a refundable deposit becomes your limit, and use it for one small recurring charge paid in full each month. Ask a family member with strong credit to add you as an authorized user on an old, well-managed card, which can lend you their account age and history. Consider a small credit-builder installment loan to add a different account type. Each of these adds positive payment history, the factor that matters most, and within a year or two of flawless behavior the difference is dramatic. The mistakes on this list are easy to make, but none of them are permanent. Your next twelve months of habits matter more to your score than any single bad month behind you.

Frequently Asked Questions

What hurts your credit score the most?

Payment history is the single most damaging factor, accounting for 35% of your FICO score. A 30-day late payment on a 780 score can cause a drop of 60 to 110 points immediately. Collections, charge-offs, and bankruptcy are also severely damaging. High credit utilization (above 30%) is the second most impactful factor and affects 30% of your score, though it resets quickly once balances are paid down.

How many points does a late payment drop your credit score?

A single 30-day late payment typically drops a score of 780 or above by 60 to 110 points. Someone with a score of 680 loses roughly 50 to 80 points. The higher your starting score, the more points you lose from the first delinquency, because the model treats it as more statistically anomalous. Late payments stay on your credit report for seven years but have the most impact in the first two years.

Does closing a credit card hurt your credit score?

Yes, for two reasons. Closing a card reduces your total available credit, which raises your credit utilization ratio even if your balances didn't change. It also lowers the average age of your accounts, which negatively affects the length of credit history factor (15% of your FICO score). The older the card, the more damage closing it causes. The best approach is to keep old cards open with occasional small purchases.

How long does it take to rebuild a credit score after damage?

Recovery time depends on the type of damage. High utilization rebounds within 1 to 2 billing cycles once balances are paid. A late payment begins to have less impact after 2 years and falls off your report after 7 years. A collection account stays for 7 years. Bankruptcy stays for 7 to 10 years. With consistent positive behavior, most people can return to the "Good" score range (670+) within 2 to 3 years after most types of damage.

How much does a hard inquiry hurt your credit score?

Each hard inquiry from a credit application typically costs 5 to 10 points and stays on your credit report for 2 years, though it only affects your score for 12 months. Multiple inquiries in a short period compound the impact. The exception is mortgage, auto loan, and student loan shopping: multiple inquiries for the same loan type within 14 to 45 days are counted as a single inquiry by FICO.

What credit utilization ratio is best for your credit score?

People with the highest FICO scores typically maintain utilization below 10% across all accounts and on each individual card. Utilization above 30% begins to noticeably hurt your score. Above 50%, the impact becomes significant. Utilization is one of the fastest factors to improve: pay down balances and your score reflects the improvement within one to two billing cycles.