What Is Net Worth and Why It's the Only Financial Number That Actually Matters

Your salary tells you how much you earn. Your net worth tells you how financially healthy you actually are. Here's why the distinction matters — and how to calculate yours today.

Ask most people how they're doing financially and they'll tell you their salary. But salary is the wrong number. It measures how much money flows past you, not how much you've actually kept, and two people earning the identical income can be in completely opposite financial situations. Net worth is the number that cuts through all of it. It is, bluntly, the only financial figure that tells the whole truth about where you stand, and calculating yours takes about ten minutes.

Net worth doesn't care what you earn, what you drive, or what your job title is. It cares about one thing: what you'd have left if you sold everything you own and paid off everything you owe. That single number reveals whether your lifestyle is built on wealth or on debt, which is why it matters more than any paycheck.

The Number That Tells the Truth

Income is a flow and net worth is a stock. Flow is the water coming through the pipe each month; stock is how much you've actually collected in the tank. A high flow with an open drain, spending and debt, fills nothing. A modest flow with a sealed tank fills steadily over time.

This is why the salary question is so misleading. A surgeon earning $400,000 who spends $410,000 has a negative net worth; a teacher earning $55,000 who saves consistently can have a positive one. The surgeon looks richer and is, in the only sense that matters, poorer. Net worth strips away the appearance of wealth and shows the substance, which is exactly why it's worth tracking when a paycheck isn't.

How to Calculate It

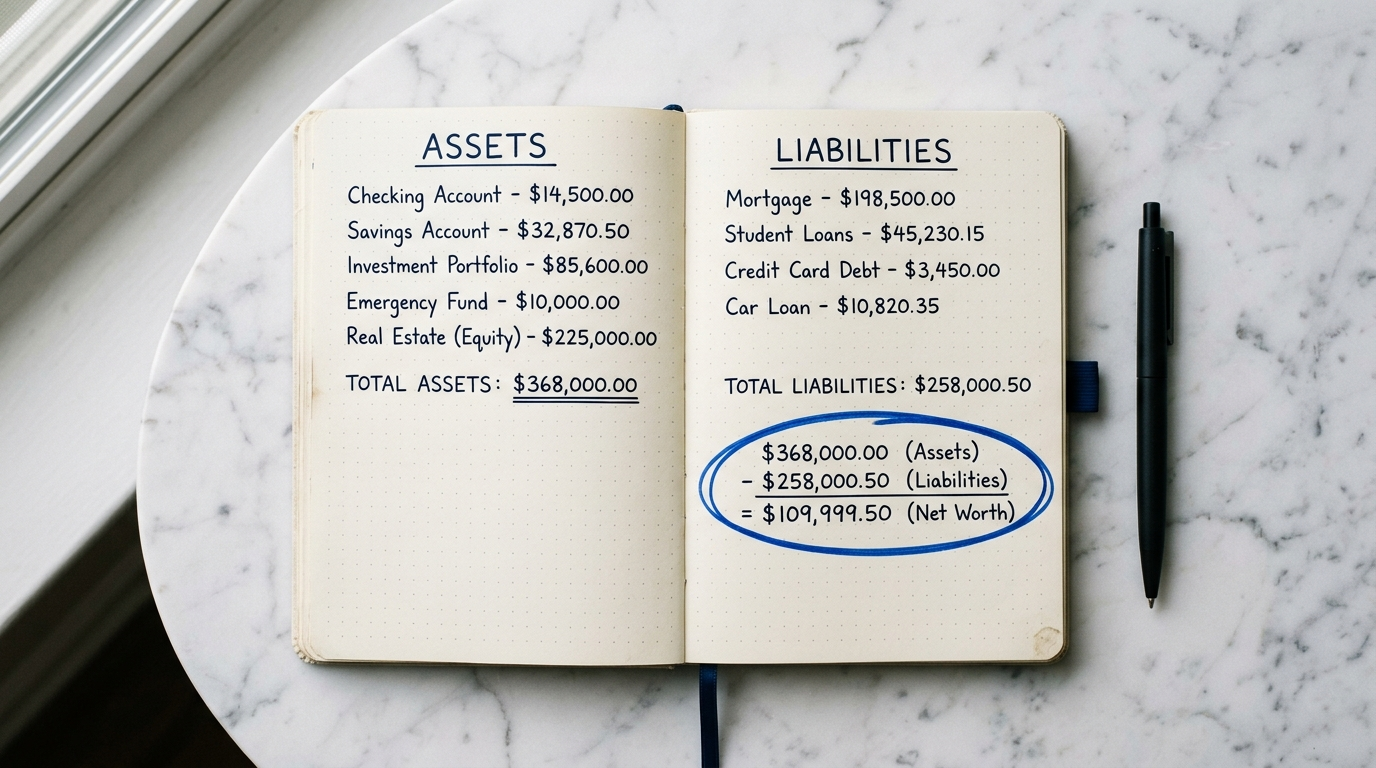

The formula is the simplest in personal finance: Net Worth = Total Assets − Total Liabilities. List everything you own and assign it a current value, list everything you owe, and subtract the second from the first. The result, positive or negative, is your net worth.

| Assets (what you own) | Liabilities (what you owe) |

|---|---|

| Cash & savings: $15,000 | Mortgage: $220,000 |

| Retirement accounts: $90,000 | Student loans: $24,000 |

| Home value: $320,000 | Car loan: $12,000 |

| Car & other: $18,000 | Credit cards: $4,000 |

| Total: $443,000 | Total: $260,000 |

In this example, net worth is $443,000 minus $260,000, or $183,000. Do this once and you have a baseline; do it every quarter and you have a trend, which matters far more than any single snapshot. The net worth calculator does the arithmetic and lets you update it over time.

What Counts as an Asset vs a Liability

An asset is anything with real resale value: cash, investment and retirement accounts, the market value of your home, and significant possessions like a car. Be honest and current with values; use what you could actually sell something for today, not what you paid or what you wish it were worth. Skip tiny items, they add noise without changing the picture.

A liability is anything you owe: mortgage, student loans, car loans, credit card balances, and any personal or medical debt. One subtlety trips people up: your home is both. Its market value is an asset, but the remaining mortgage is a liability, and only the difference, your equity, actually counts toward your wealth. Counting the full home value while ignoring the mortgage is the most common way people overestimate their net worth.

Average Net Worth by Age

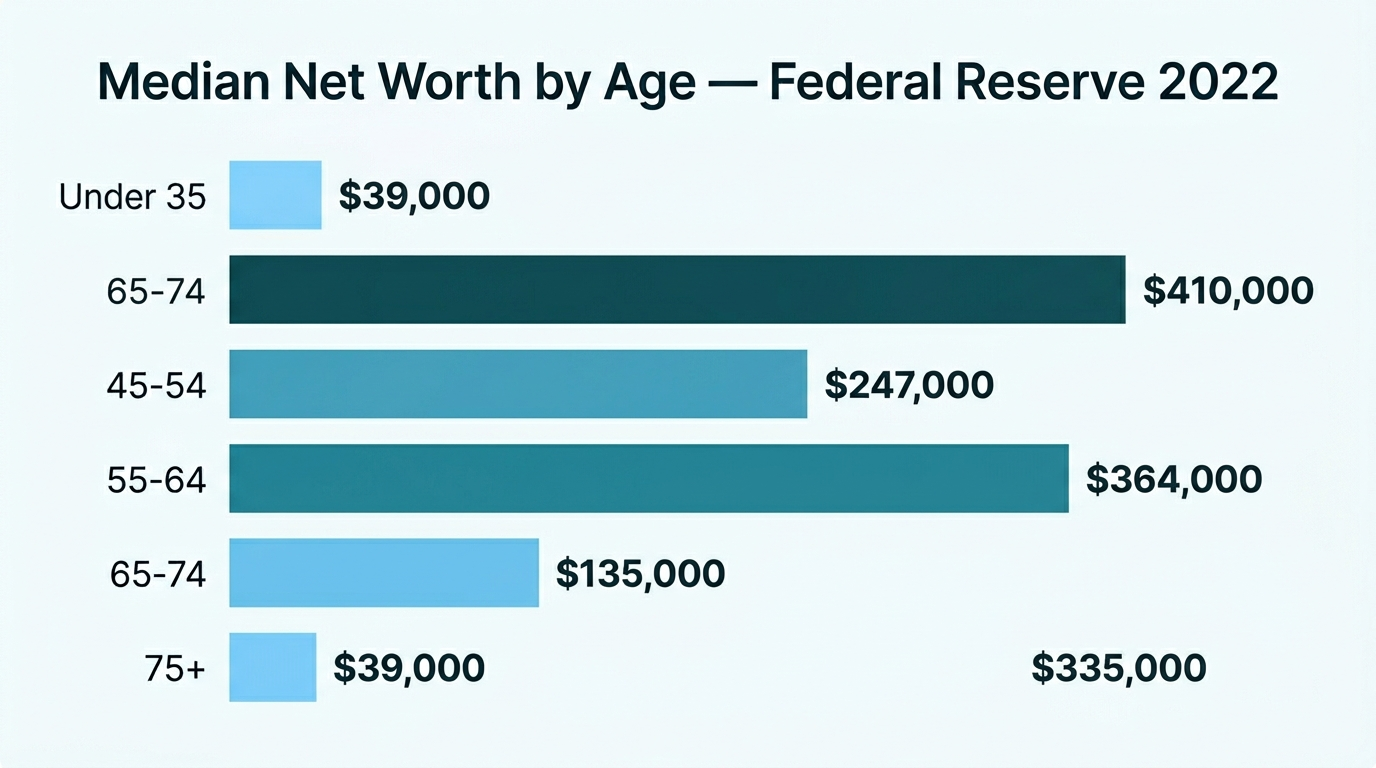

Once you know your number, it's natural to ask how it compares. Here are approximate median figures by age from Federal Reserve data, useful as a rough reference rather than a target to obsess over.

| Age group | Median net worth |

|---|---|

| Under 35 | ~$39,000 |

| 35 to 44 | ~$135,000 |

| 45 to 54 | ~$247,000 |

| 55 to 64 | ~$365,000 |

| 65 to 74 | ~$410,000 |

Treat these as context, not a verdict. Medians vary enormously by region, profession, and life choices, and the only comparison that truly matters is you against your own past. A net worth that climbs each year means you're winning, regardless of where you sit on this table.

Is Negative Net Worth Bad?

Not necessarily, and this surprises people. Negative net worth is completely normal early in life, especially with student loans or a new mortgage. A 27-year-old with a $40,000 student loan and few assets has a negative net worth on paper while being perfectly on track. The number is a snapshot, and snapshots early in a journey look different from snapshots near the destination.

What matters is the direction. A negative net worth shrinking toward zero, then climbing positive, is a success story in progress. A positive net worth quietly eroding is a warning even if the absolute number still looks fine. Always read net worth as a trend line, not a single frame.

Common Net Worth Mistakes

Calculating net worth is simple, but a few errors distort the number and rob it of its usefulness. Avoiding them keeps your figure honest, which is the whole point of tracking it.

- Counting the home's full value but forgetting the mortgage. Only your equity, value minus the loan balance, is real net worth. This is the most common way people overstate their wealth.

- Inflating possessions. Your car, furniture, and gadgets are worth what you could sell them for today, not what you paid. Most depreciate fast, so be conservative.

- Including things with no resale value. Sentimental items and most personal belongings don't belong on the asset side. If you wouldn't sell it for cash, leave it out.

- Obsessing over comparisons. Measuring your number against a friend's or an average is a fast route to bad decisions. The only meaningful comparison is you versus your past self.

A net worth figure is only as useful as it is honest. Slightly understating your assets and fully counting your debts gives you a conservative number you can trust, which beats a flattering one that lulls you into thinking you're further ahead than you are. The goal is an accurate scoreboard, not a high score.

How to Grow It and Track It

Growing net worth comes down to two levers, and only two: increase assets or decrease liabilities. Save and invest more on one side, pay down debt on the other. Every financial decision ultimately routes through one of these two paths, which is why net worth is such a clarifying number; it tells you whether what you're doing is actually working.

The habit that builds wealth is simply measuring this number regularly and watching it rise. What gets measured gets managed. This is also a natural fit for the built-in AI assistant on the calculator pages: enter your assets and debts and ask something like "my net worth is $40,000 at age 30, am I on track and what should I prioritize," and it puts your number in context and points to the next move. Track your salary if you like, but track your net worth if you want the truth. It's the one number that can't be faked, and the one that actually measures whether you're getting ahead.

Frequently Asked Questions

What is net worth?

Net worth is the total value of everything you own (assets) minus everything you owe (liabilities). The formula is: Net Worth = Total Assets − Total Liabilities. It is the single most accurate measure of your financial health.

What is the average net worth by age in the US?

According to the Federal Reserve, median net worth is approximately $39,000 for under 35, $135,000 for ages 35–44, $247,000 for ages 45–54, $365,000 for ages 55–64, and $410,000 for ages 65–74.

Is a negative net worth bad?

Not necessarily. Negative net worth is common early in life due to student loans or mortgages. What matters is the trend — if your net worth improves each year, you are moving in the right direction.

How often should I calculate my net worth?

Calculate your net worth at least once a year, ideally every quarter. Regular tracking helps you spot financial problems early and measure whether your saving and investment habits are working.

What is the difference between income and net worth?

Income is a flow — money coming in each month. Net worth is a stock — the total accumulated value you have built over time. A high income with high spending and debt can produce a lower net worth than a moderate income with disciplined saving.