401(k) vs Roth 401(k): Which Should You Choose and Does It Really Matter?

Both accounts deliver the same tax benefit in different orders. The entire decision comes down to one question: will your tax rate be higher now or in retirement? Here's the complete math, the honest framework, and the answer most guides skip.

The 401(k) versus Roth 401(k) decision feels enormous, so people agonize over it, then often pick based on a vague feeling. Here's the freeing truth: the two accounts deliver the exact same tax benefit, just in opposite order, and the entire choice collapses to a single question. Will your tax rate be higher now or in retirement? Answer that honestly and the "right" account becomes obvious. This is the complete math, the honest framework, and the part most guides skip.

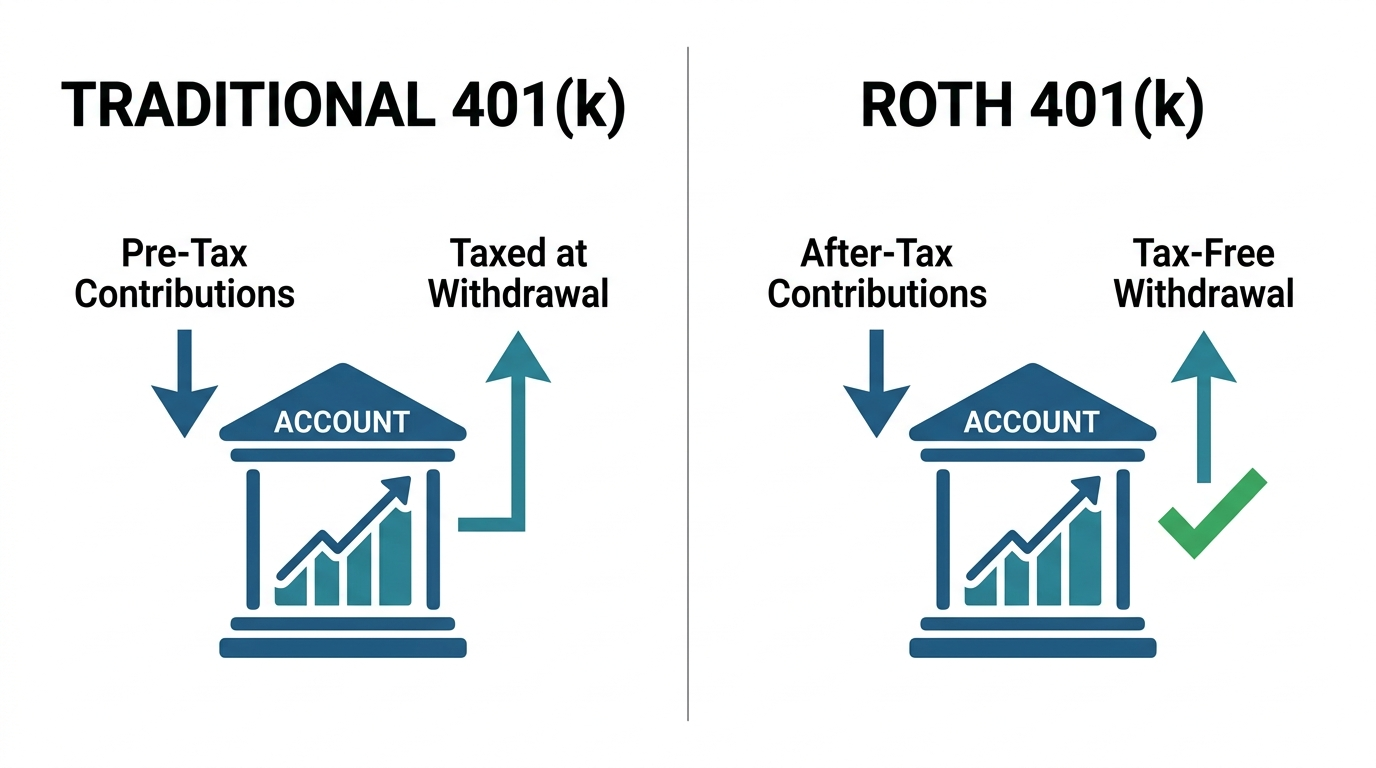

Both are employer retirement accounts with the same contribution limits and the same investment options. The only difference is when the government taxes the money: on the way in, or on the way out. Everything that follows flows from that one distinction, so let's make it concrete.

Same Benefit, Opposite Order

A traditional 401(k) is pre-tax. You contribute before the IRS takes its cut, so you get a deduction today, your money grows untaxed, and you pay ordinary income tax on every dollar you withdraw in retirement. A Roth 401(k) is after-tax. You contribute money you've already paid tax on, get no deduction today, and then every dollar you withdraw in retirement, including all the growth, is completely tax-free.

One taxes the seed; the other taxes the harvest. Traditional skips the tax now and pays it later. Roth pays the tax now and skips it later. Neither is inherently better. Which one wins depends entirely on whether your tax rate is higher in the year you contribute or in the year you withdraw.

The Only Question That Matters

Strip away the noise and the decision is just a tax-rate bet. If your tax rate will be lower in retirement than it is now, the traditional 401(k) wins, because you avoid tax at today's high rate and pay it later at a low one. If your tax rate will be higher in retirement, the Roth wins, because you pay tax now at a low rate and escape the higher one later.

That single comparison drives the whole choice. A high earner in their peak years likely faces a lower rate in retirement, favoring traditional. A young worker early in their career, or anyone who expects rising income, may face a higher rate later, favoring Roth. Estimate your likely retirement bracket against your current one with help from the income tax calculator before you assume which way you lean.

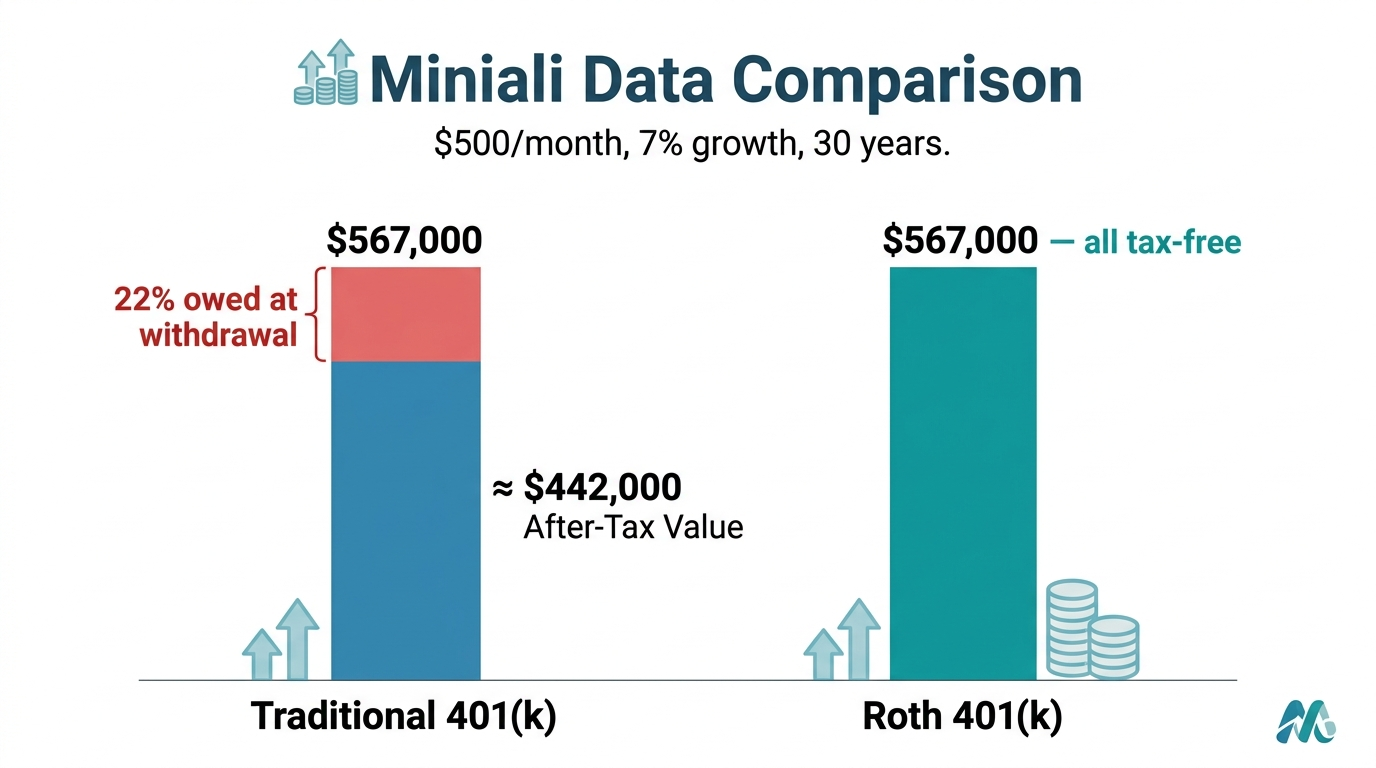

The Math When Rates Are Equal

Here's the part that surprises people: if your tax rate is identical now and in retirement, the two accounts produce exactly the same amount of spendable money. Watch it work with a 22% rate both now and later, $10,000 of pre-tax income, and 30 years of 7% growth.

| Step | Traditional | Roth |

|---|---|---|

| Amount invested | $10,000 (pre-tax) | $7,800 (after 22% tax) |

| After 30 years at 7% | $76,100 | $59,358 |

| Tax at withdrawal (22%) | −$16,742 | $0 |

| Spendable in retirement | $59,358 | $59,358 |

Identical to the dollar. This is the math most arguments ignore, and it proves the point: the accounts only diverge when the tax rates differ. Everything else, the "tax-free growth" of the Roth and the "tax deduction" of the traditional, is the same benefit described from two ends. Model your own numbers with the 401(k) calculator and a Roth comparison on the Roth IRA calculator.

When Traditional Wins and When Roth Wins

Because the decision is a tax-rate bet, the guidance follows directly. Traditional tends to win when you're in a high bracket now and expect a lower one in retirement, which fits many mid-to-late career high earners. The upfront deduction is worth the most when your current rate is high.

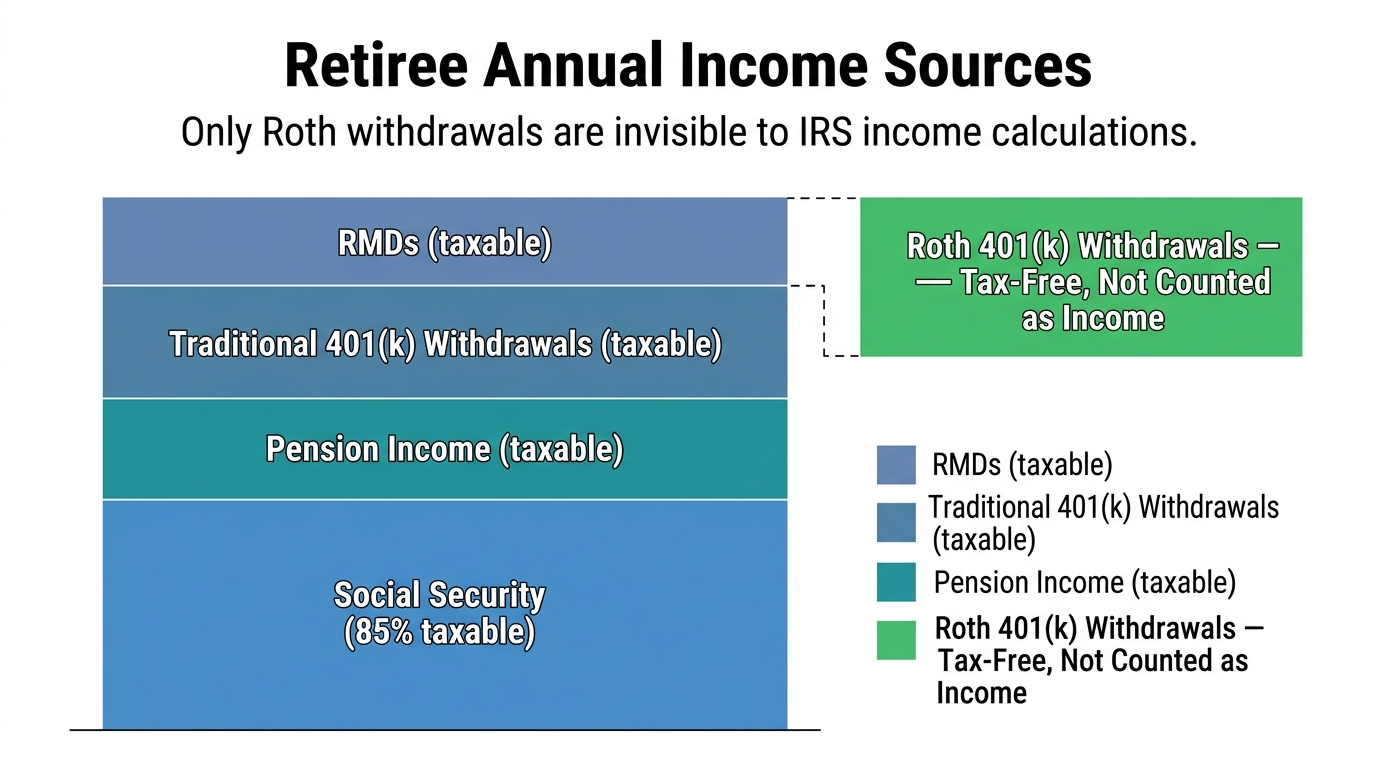

Roth tends to win in the opposite cases. If you're early in your career, in a low bracket, or you expect your income, and possibly future tax rates generally, to be higher later, paying tax now at a low rate is the bargain. Roth also carries a quiet advantage: tax-free withdrawals don't inflate your taxable income in retirement, which can help keep more of your Social Security untaxed and your Medicare premiums lower. Those second-order effects often tip genuinely close calls toward Roth.

Why Splitting Is Often the Smart Play

Here's the honest part most guides won't say: you can't know your future tax rate with certainty. Tax law changes, careers take unexpected turns, and retirement income is hard to predict decades out. When you genuinely can't tell which bracket will be higher, the strongest move is often to hedge by contributing to both.

Splitting your contributions between traditional and Roth gives you tax diversification: some money you'll pay tax on later, some you won't. In retirement, that lets you pull from whichever account is more tax-efficient in a given year, controlling your taxable income with a flexibility that an all-traditional or all-Roth saver simply doesn't have. You're allowed to divide your contributions in any proportion, as long as the combined total stays within the annual IRS limit. For many people, "some of each" is not a cop-out; it's the genuinely optimal answer to real uncertainty.

The Details That Tip the Scale

A few specifics matter once you've settled the big question. They can nudge a close decision or change how you execute it.

- The employer match is always pre-tax. Even if you contribute to a Roth 401(k), your company's match lands in a traditional bucket. So you'll have some traditional money regardless, which is another small argument for leaning Roth on your own contributions.

- Roth 401(k)s no longer have lifetime RMDs. Since the SECURE 2.0 Act, Roth 401(k) accounts skip required minimum distributions during your lifetime, letting the money compound tax-free longer.

- Job changes preserve the status. You can roll a Roth 401(k) into a Roth IRA and a traditional 401(k) into a traditional or Roth IRA when you leave, keeping the tax treatment intact.

- Capture the full match first. Before optimizing traditional versus Roth, contribute enough to get every dollar of employer match. That match is an instant return no tax strategy can beat.

A Common Point of Confusion: Roth 401(k) vs Roth IRA

People often blur the Roth 401(k) and the Roth IRA together because both offer tax-free withdrawals, but they're different accounts with different rules, and knowing which is which prevents real mistakes.

The Roth 401(k) lives inside your employer's plan. It has the same high contribution limit as a traditional 401(k), receives the employer match (in a separate pre-tax bucket), and has no income limit, so even high earners can use it. The Roth IRA is a separate account you open yourself, with a much lower annual contribution limit and income caps that phase out high earners entirely. Many people use both: the Roth 401(k) for the high limit and the match, and a Roth IRA on the side for its wider investment choices and flexibility.

The practical sequence for most savers is straightforward. Contribute enough to the 401(k) to capture the full employer match first, since that's free money. Then, if eligible, fund a Roth IRA for its flexibility. Then return to the 401(k) to push toward the annual limit. Mixing up the two accounts, or assuming the Roth IRA's income limits also apply to the Roth 401(k), is a common error that can cost you access to the better option for your situation.

Run Your Own Numbers

The 401(k) versus Roth 401(k) choice is genuinely simpler than its reputation. Decide whether your tax rate is likely higher now or in retirement, pick accordingly, and split the difference when you honestly can't tell. Then make sure you're saving enough overall, which matters far more than the traditional-versus-Roth detail.

This is also a great question for the built-in AI assistant on the calculator pages. Tell it something specific like "I'm 28, in the 12% bracket, and expect to earn much more later, traditional or Roth," and it reasons through your likely tax trajectory instead of giving a one-size answer. Confirm you're on track for the bigger picture with the retirement calculator. The account type is a meaningful optimization, but the amount you contribute is the decision that actually builds the retirement.

Frequently Asked Questions

What is the difference between a 401(k) and a Roth 401(k)?

A traditional 401(k) uses pre-tax contributions: you get a tax deduction now and pay taxes on withdrawals in retirement. A Roth 401(k) uses after-tax contributions: no tax deduction now, but all qualified withdrawals in retirement are completely tax-free including all growth.

Which is better, a traditional 401(k) or a Roth 401(k)?

It depends on your tax rate now versus retirement. If you're in a lower bracket now and expect higher income later, Roth is typically better. If you're in a high bracket now and expect lower income in retirement, traditional is typically better. When uncertain, splitting between both is a strong strategy.

Can I contribute to both a traditional 401(k) and a Roth 401(k) in the same year?

Yes. You can split your contributions between traditional and Roth in any proportion, as long as your total contributions across both don't exceed the annual IRS limit: $23,000 in 2024, or $30,500 if you're 50 or older.

Do Roth 401(k) accounts have required minimum distributions?

Since the SECURE 2.0 Act, Roth 401(k) accounts no longer require minimum distributions during the owner's lifetime, the same as Roth IRAs. This makes them particularly valuable for people who don't need the money in early retirement and want to let it compound longer.

What happens to a Roth 401(k) when I change jobs?

You can roll a Roth 401(k) into a Roth IRA or into a new employer's Roth 401(k) if the new plan accepts rollovers. The tax-free status is preserved. Rolling into a Roth IRA also eliminates RMDs permanently, which is often beneficial.