Term Life Insurance vs Whole Life: Why the Math Favors One Every Time

A healthy 35-year-old pays $28/month for term life and $500/month for whole life with the same death benefit. Here's what happens to the $472 difference when you invest it, and why the math lands the same way almost every time.

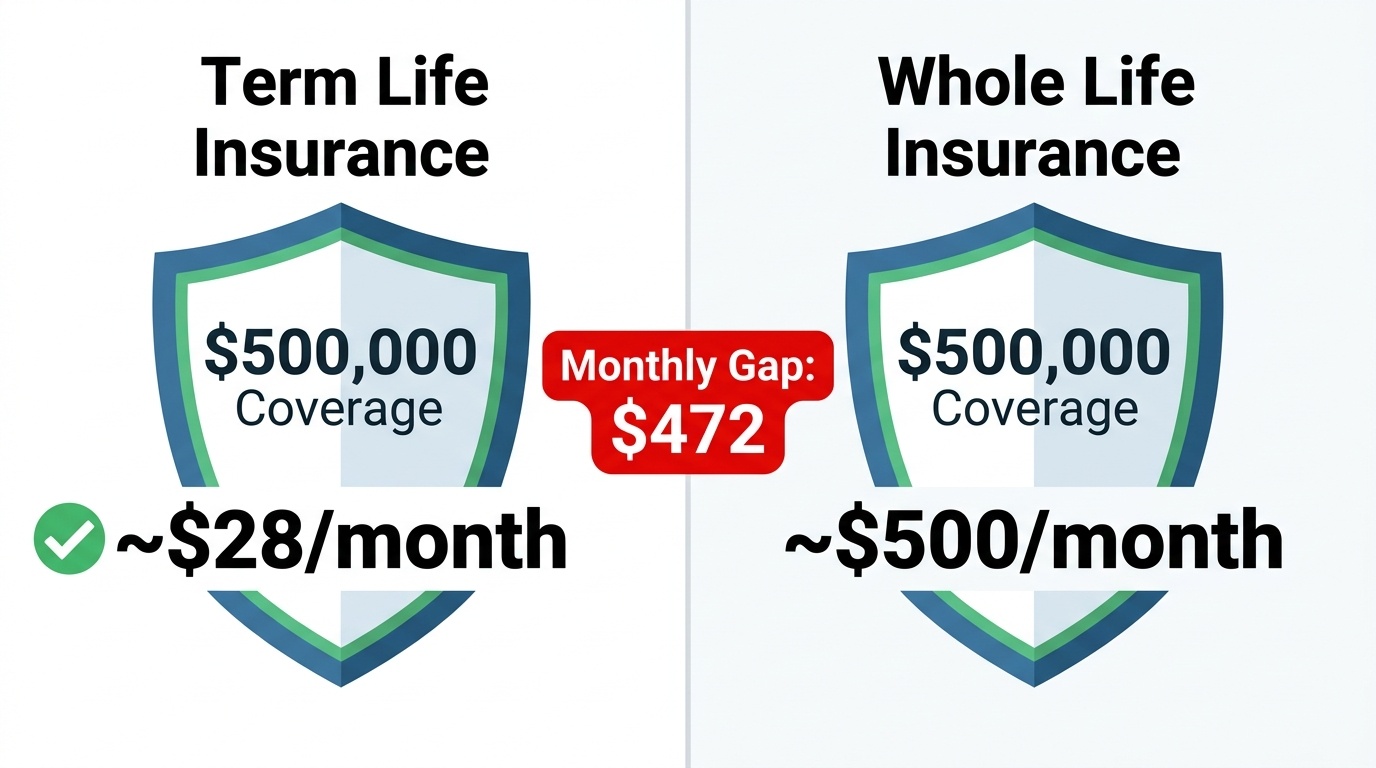

A healthy 35-year-old can buy $500,000 of term life insurance for around $28 a month. The same coverage as whole life runs roughly $500 a month. That's not a typo, and it's the single most important fact in the entire term-versus-whole-life debate. Once you understand where that $472 monthly difference goes, and what happens if you invest it instead, the math lands the same way for the overwhelming majority of people, almost every single time. Here's the honest comparison the sales pitch leaves out.

Life insurance exists to do one job: replace your income if you die while people depend on it. Term insurance does exactly that job and nothing else. Whole life bundles that job with a savings-and-investment product, and the bundle is where the cost, and the confusion, comes from. Let's separate the two cleanly.

The Two Kinds of Life Insurance

Term life insurance covers you for a set period, usually 10, 20, or 30 years, and pays out only if you die during that window. It's pure insurance: cheap, simple, and temporary. When the term ends, so does the coverage, which is the point. By then your kids are grown, the mortgage is gone, and you no longer need it.

Whole life insurance covers you for your entire life and includes a cash value account that grows slowly over time. It never expires, and you can borrow against the cash value. That permanence and savings feature is why it costs roughly ten to twenty times more than term. The question is whether what you get for that enormous premium is worth it, and for most people the answer is no.

The Price Gap Is Staggering

Numbers make the gap concrete. For a healthy 35-year-old buying $500,000 in coverage, the two options look like this.

| Term (20-year) | Whole life | |

|---|---|---|

| Monthly premium | ~$28 | ~$500 |

| Coverage length | 20 years | Lifetime |

| Builds cash value | No | Yes, slowly |

| Monthly difference | ~$472 freed up to invest | |

That $472 a month is the heart of the decision. With whole life, it disappears into premiums. With term, it's yours to do something else with, and what you do with it is where the real wealth gets built.

Buy Term and Invest the Difference

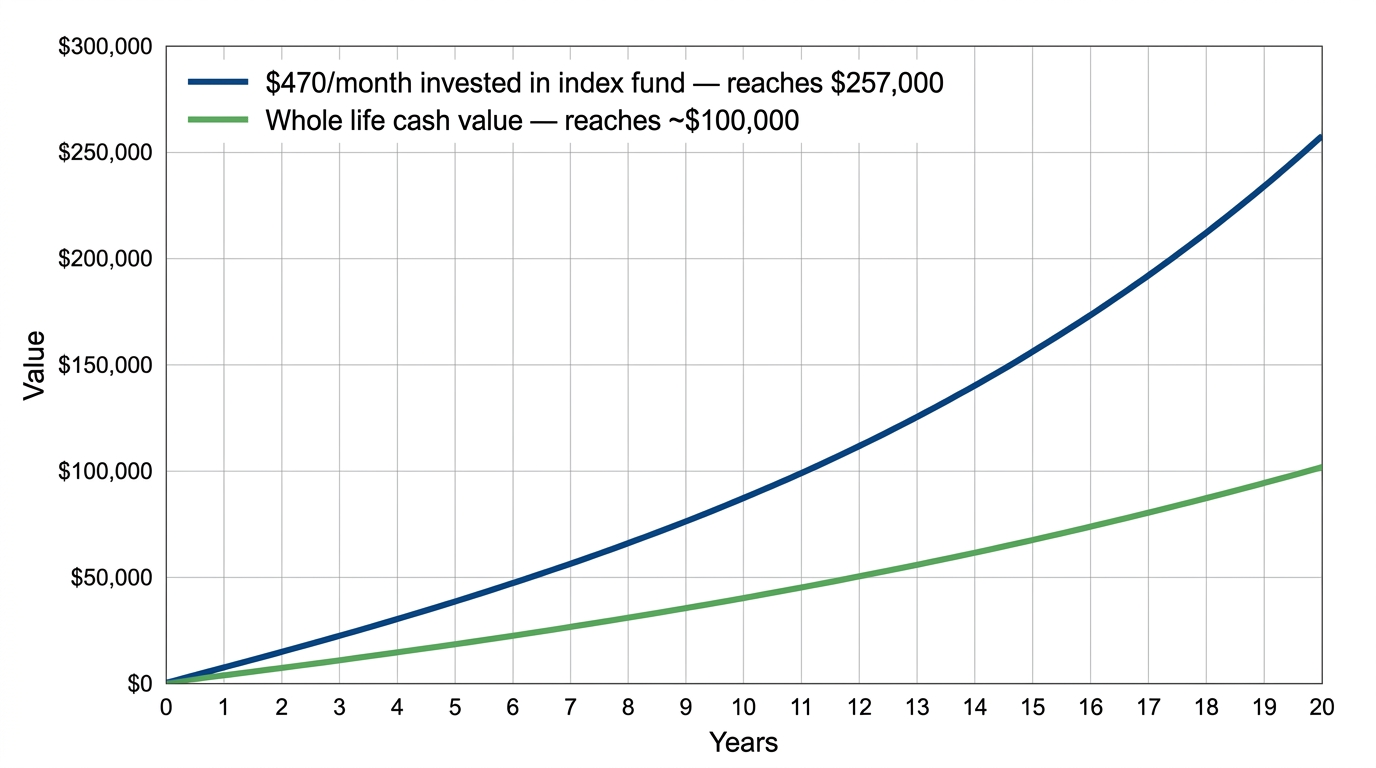

The strategy that follows is so well known it has a name: "buy term and invest the difference." You purchase cheap term coverage for the years you actually need protection, then invest the premium you saved versus whole life. Over time, that invested difference typically grows into far more than a whole life policy's cash value.

Run the numbers. Investing that $472 a month at a 7% annual return for 20 years produces roughly $245,000. You spent the same total each month as the whole life buyer, but instead of handing it to an insurer, you built a quarter-million-dollar investment account that's entirely yours, fully liquid, and not locked behind insurance-company rules. Model your own version with the investment calculator or the compound interest calculator, and the gap becomes undeniable.

The Real Return on Whole Life

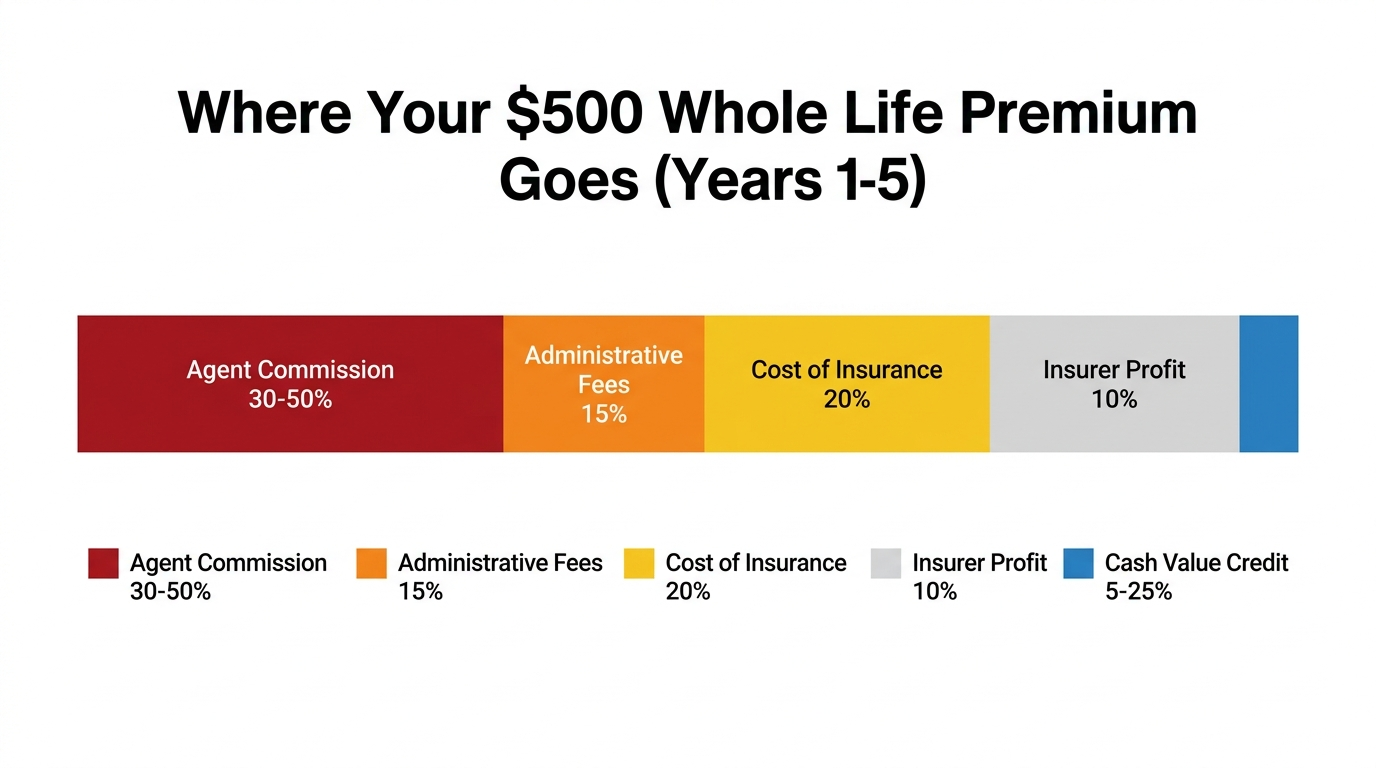

Whole life is sold as an investment, so judge it as one. Measured purely as an investment, the internal rate of return on most whole life policies runs between roughly 1.5% and 3.5% a year over the first couple of decades. Compare that to the stock market's long-run real return of around 7%, and the gap is enormous and compounding.

The reason is structural, not bad luck. Agent commissions, administrative fees, and the insurer's profit margin consume a large share of your early premiums before anything reaches the cash value account. That's why whole life cash value barely moves in the first years; you're paying for the overhead first. A product returning 2% while a simple index fund returns 7% isn't a savings vehicle; it's an expensive way to underperform. Compare returns honestly with the ROI calculator before you believe the illustration an agent shows you.

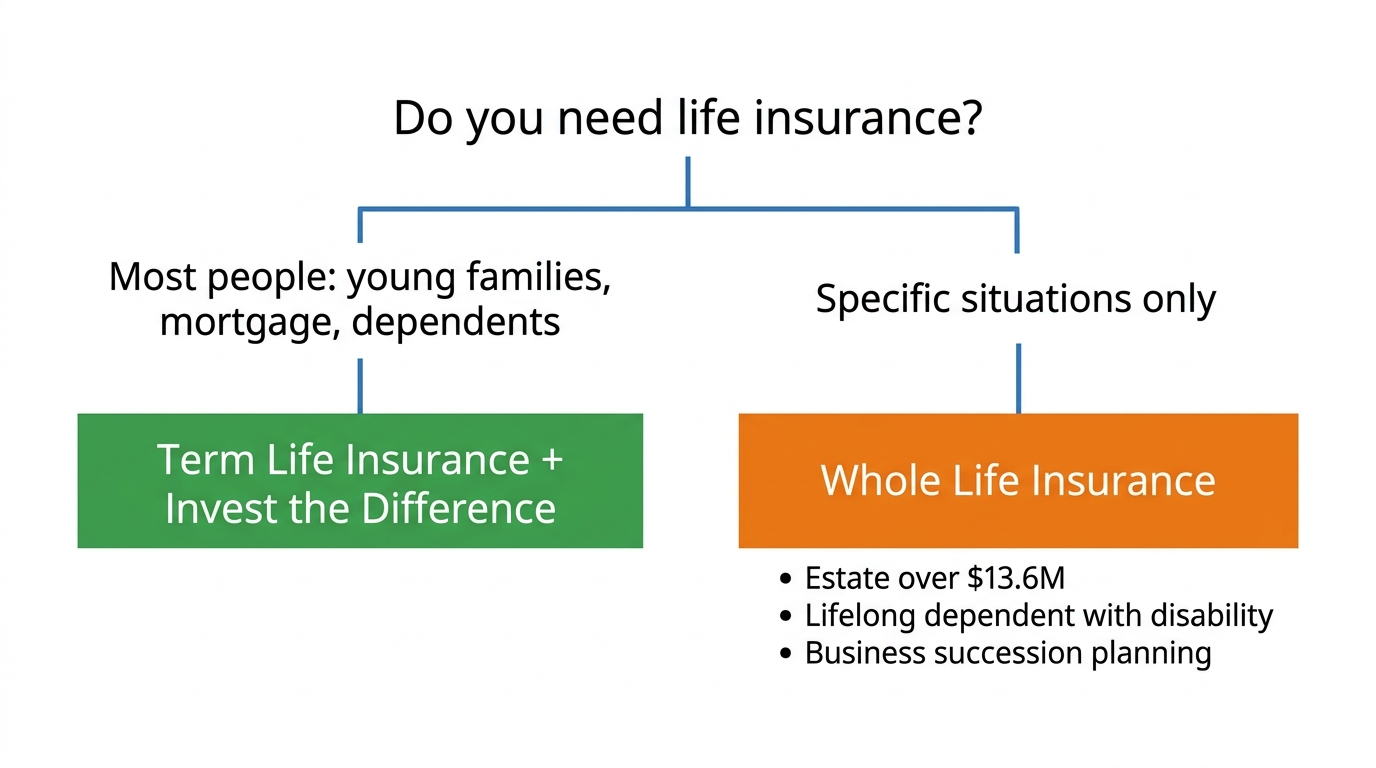

When Whole Life Actually Makes Sense

Whole life isn't a scam, and there are genuine cases where it's the right tool. Being honest about them is what separates analysis from a rant. Whole life can make sense for estate planning when you have a taxable estate in the millions, for providing lifelong coverage to a dependent with a disability, for certain business succession arrangements, or for locking in insurability when a health condition makes future coverage uncertain.

Notice what those cases have in common: they're specific, relatively uncommon situations, usually involving significant wealth or special circumstances. For the typical person whose goal is simply protecting their family during their working years, none of them apply. If you're not in one of these situations, the math overwhelmingly favors term plus investing. Don't let a rare valid use case talk you into a product you don't need.

Watch for These Whole Life Sales Tactics

Whole life is sold hard because it pays the agent a large commission, often a big chunk of your first year's premium. That incentive shapes the pitch, so it helps to recognize the common lines before you're sitting across from someone using them.

- "It's forced savings." True, but it's forced savings into a product returning 2%. A simple automatic transfer into an index fund is also forced savings, at a far better return.

- "Term is renting; whole life is owning." A catchy analogy with no math behind it. Insurance isn't a home, and the comparison exists to make a worse return sound responsible.

- "You can borrow against the cash value." You can, but you're borrowing your own money and often paying interest to do it. That's not a benefit unique to a good investment.

- "Markets are risky; this is guaranteed." The "guarantee" is a low return locked in by high fees. Over decades, a diversified portfolio's risk is far smaller than the guaranteed cost of underperformance.

None of these are lies exactly, but each is engineered to make an expensive, low-return product feel safe and smart. When you hear them, return to the one number that cuts through everything: the internal rate of return. A product that grows your money at 2% while charging you ten times the price of pure protection is not a savings plan, however it's framed. Ask any agent to show you the policy's guaranteed IRR over 20 years in writing, and watch how the conversation changes.

How Much Coverage Do You Actually Need

Once you've chosen term, size it correctly. A common starting guideline is 10 to 12 times your annual income, but a sharper approach adds up what your family would actually need: the outstanding mortgage, remaining years of income replacement until your youngest child is independent, all other debts, and future costs like education.

Match the term length to your period of real vulnerability, typically the years you have dependents at home and a mortgage to pay. A 30-year-old parent with young kids and a new mortgage might choose 30-year term; someone closer to financial independence might need only 20. Look for a policy with a convertibility option, which lets you switch to permanent coverage later without a new medical exam, the one feature that quietly covers the rare scenario where whole life turns out to be genuinely needed.

Make the Call

For the vast majority of people, the decision is clear: buy enough term insurance to protect the years your family depends on your income, and invest the large difference you save versus whole life. You end up with the same protection and a substantial investment account, instead of an expensive policy returning 2%.

This is a great question for the built-in AI assistant on the calculator pages. Tell it something like "I'm 35 with two kids and a mortgage, how much term life do I need and what happens if I invest the difference versus buying whole life," and it walks through your coverage need and the long-term math side by side. The insurance industry profits when the decision feels complicated. The honest version is simple, and now you have it.

Frequently Asked Questions

What is the difference between term life and whole life insurance?

Term life insurance provides coverage for a set number of years (typically 10, 20, or 30) and pays a death benefit only if you die during that period. Whole life insurance provides permanent coverage with no expiration and includes a cash value savings component that grows over time. Term premiums are dramatically lower: a 35-year-old pays roughly $28/month for $500,000 of 20-year term coverage versus $400 to $600/month for an equivalent whole life policy.

Is whole life insurance ever worth it?

Whole life makes financial sense in specific situations: estate planning for individuals with taxable estates above $13.61 million, providing permanent coverage for a lifelong dependent with a disability, business succession planning under a buy-sell agreement, or locking in insurability when a health condition makes future coverage uncertain. For most people in none of these situations, the math consistently favors buying term and investing the premium difference.

What is the "buy term and invest the difference" strategy?

Buy term and invest the difference means purchasing a low-cost term life policy and directing the premium savings versus whole life into an investment account. For example, choosing $30/month term over $500/month whole life frees $470/month. Invested at 7% annual return over 20 years, that becomes approximately $257,000, which typically exceeds the cash value accumulated inside a comparable whole life policy over the same period.

What is the internal rate of return on a whole life insurance policy?

The internal rate of return on most whole life policies, measured purely as an investment, runs between 1.5% and 3.5% per year over the first 20 years. This compares unfavorably to historical stock market returns of roughly 7% annually in real terms after inflation. The gap is structural: agent commissions, administrative fees, and insurer profit margins consume a large share of early premiums before anything reaches the cash value account.

How much term life insurance coverage do I need?

A common starting guideline is 10 to 12 times your annual income. A more precise calculation accounts for your outstanding mortgage balance, number of years until your youngest child is financially independent, all outstanding debts, and the annual income replacement your surviving spouse would need. Match the term length to your period of peak financial vulnerability, typically the years when you have dependents and an outstanding mortgage.

Can I convert a term life policy to whole life later?

Many term life policies include a convertibility option allowing you to convert to permanent coverage before the term expires without a new medical exam or health underwriting. This feature is valuable if your health changes during the term and you later need permanent coverage. Check for this option when comparing policies, as it addresses the main scenario where whole life is genuinely needed without requiring it from the start.