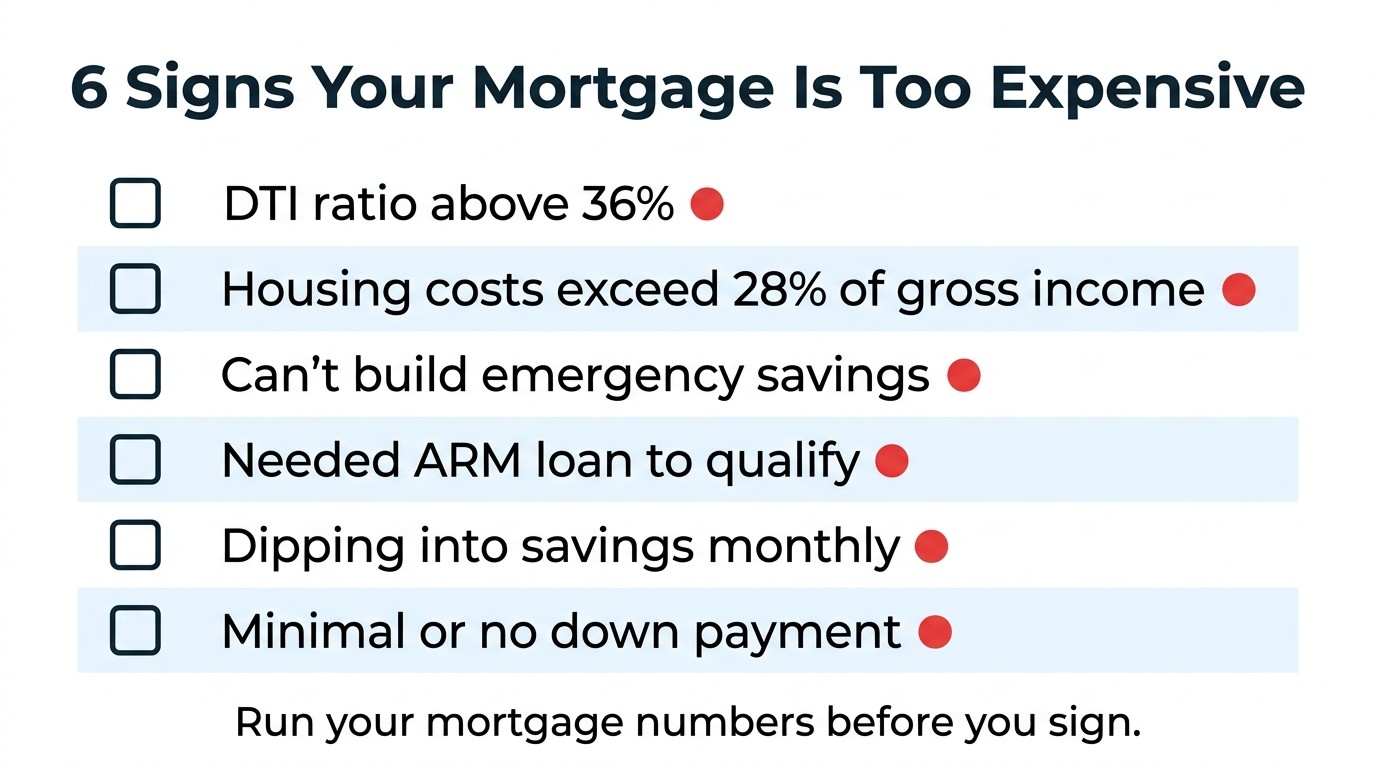

6 Signs Your Mortgage Is Too Expensive for Your Income And What to Do

Lenders approve loans based on the maximum you can technically repay, not on what keeps you financially comfortable. These six benchmarks show you whether your mortgage is stretched past what your income can comfortably support.

A bank approving your mortgage is not the same as you being able to afford it. Lenders calculate the maximum you can technically repay without defaulting; they do not calculate what leaves you able to save, handle an emergency, and still have a life. That gap is where "house poor" lives, and millions of people sign for a mortgage that's too expensive without realizing it until the savings account stops growing. Here are six clear signs your mortgage is stretched past what your income can comfortably carry, and what to do about each one.

The encouraging part is that every one of these signs is measurable. You don't have to guess whether your housing costs are too high; you can check them against specific thresholds. If several of these apply to you, it's not a moral failing or a reason to panic. It's a signal to adjust, and there are real moves available no matter which stage you're at.

Sign 1: Housing Eats More Than 28% of Your Income

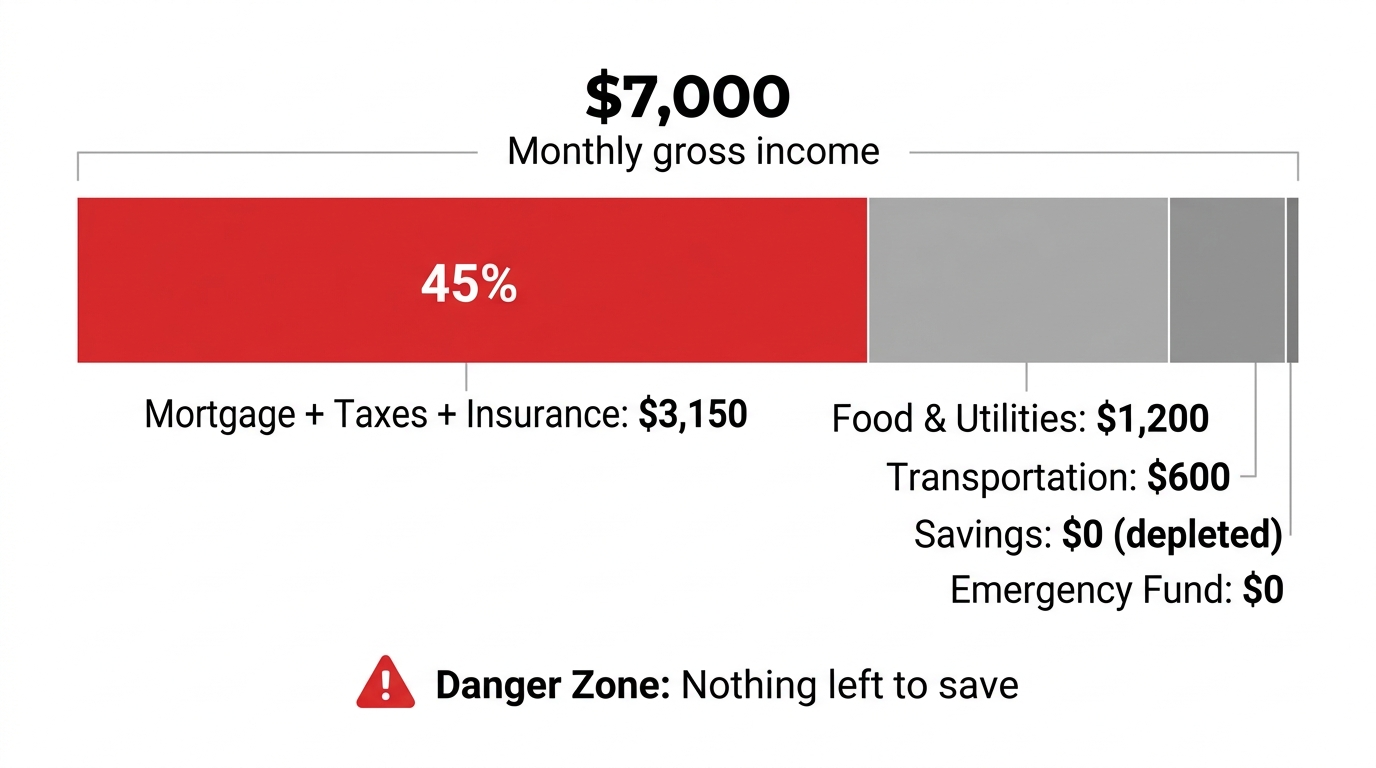

The classic guideline is that total housing costs, principal, interest, property taxes, and insurance, should stay at or below 28% of your gross monthly income. That's the front-end ratio, and lenders use it, but it has a catch: it's based on gross pay, the number before taxes and deductions.

You don't pay your mortgage with gross pay. A more honest personal check is keeping housing under about 35% of your actual take-home income. On a $6,000 gross monthly income, 28% is $1,680, but if your take-home is $4,500, that same payment is already 37% of the money you actually receive. If housing is swallowing more than a third of your take-home pay, the budget is tight before a single other bill arrives. Test your real number against the price you're considering with the house affordability calculator.

Sign 2: Your Total Debt-to-Income Ratio Is Above 36%

Your debt-to-income ratio is the share of your gross monthly income consumed by all minimum debt payments combined: the mortgage plus car loans, student loans, and credit card minimums. Lenders will approve you up to a 43 to 50% DTI, which is precisely the problem. Approval at that level leaves almost no room to breathe.

Financial planners consistently recommend keeping total DTI at or below 36%. Below 20% is excellent. Once you're past 43%, a large portion of every paycheck is already spoken for by debt before you buy groceries or save a dollar. Check yours on the debt-to-income ratio calculator; if the mortgage pushes the total above 36%, the house is leaning on the rest of your financial life to stay standing.

Sign 3: You Can't Save While Paying It

This is the most practical test of all, and it cuts through every ratio. If your mortgage is current but your savings haven't grown in months, your housing cost is too high for your income, no matter what the percentages say. A home you're technically paying for while making zero financial progress everywhere else is the textbook definition of being house poor.

Healthy finances mean the mortgage is paid and money still flows into retirement, an emergency fund, and goals. If every spare dollar disappears into the house, you've bought an expensive trap rather than an asset. Saving nothing for years while servicing a mortgage can leave you worse off than a renter who invested the difference, even though you "own."

Sign 4: One Emergency Would Make You Miss a Payment

A mortgage is affordable only if you can absorb a shock without it collapsing. If a car repair, a medical bill, or a few weeks between jobs would put your payment at risk, the mortgage is consuming the financial cushion you need to stay safe.

The benchmark is an emergency fund of three to six months of essential expenses, including the mortgage, sitting in accessible savings. If buying the home wiped out your savings or the payment is too high to ever rebuild them, you're living one surprise away from a missed payment. That fragility is itself a sign the house costs more than your income can safely support, regardless of whether the monthly number "fits" on paper.

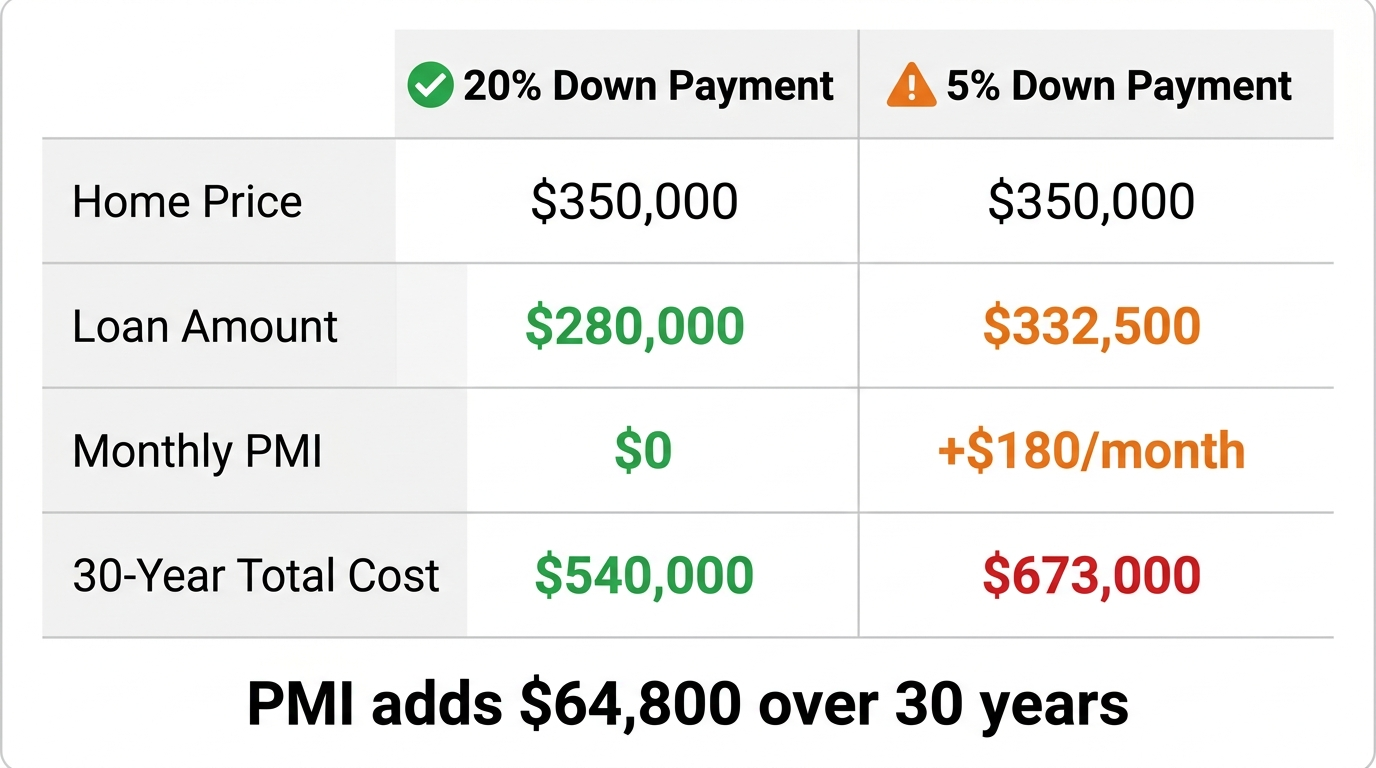

Sign 5: A Small Down Payment Is Stretching You Thin

Putting less than 20% down is not automatically a mistake, but it carries a cost worth seeing clearly. It triggers private mortgage insurance, adding $100 to $300 a month that benefits the lender, not you. It also means a larger loan, a higher payment, and a thinner equity cushion if prices dip.

The warning sign is when a minimum down payment was chosen not strategically but because there simply wasn't more saved, and the resulting payment is already a stretch. That combination, little equity and a tight payment, is fragile: if values fall, you can end up owing more than the home is worth with no savings to ride it out. Model how the down payment size changes your monthly cost with the mortgage calculator before you commit.

Sign 6: You're Using Credit to Cover Monthly Gaps

The final and most urgent sign: if you're leaning on credit cards to cover ordinary monthly expenses because the mortgage ate the budget, the situation has already tipped. You're effectively borrowing at 20%-plus interest to subsidize a house, which compounds the problem every month.

This pattern often hides behind a current mortgage. The payment goes out on time, so it looks fine, while credit card balances quietly climb to fill the gap the mortgage created. Carrying growing card balances while house-rich and cash-poor is a flashing warning that housing costs have outrun income, and it's the sign that most demands immediate action.

Why Lenders and You Are Solving Different Problems

Underneath all six signs is one structural truth worth understanding: the bank and you are not trying to answer the same question. The lender is calculating the largest loan you can carry with an acceptably low chance of default. You should be calculating the payment that still lets you build wealth and absorb life's surprises. Those are very different targets.

A lender is comfortable if you can technically make the payment, even if doing so consumes nearly everything else. Default risk is their concern; your retirement savings and your stress level are not on their spreadsheet. This is why "we got approved for more than we expected" is a trap dressed up as good news. The approval number is the edge of the cliff, not the safe distance from it.

The fix in mindset is to flip the order. Decide what monthly payment leaves room to save 15 to 20% of your income, fund emergencies, and live, then work backward to the price that produces it. That number is almost always below the approval ceiling, sometimes far below. Buying at the figure that protects the rest of your financial life, rather than the maximum the bank will lend, is the single most reliable way to avoid every sign on this list.

What to Do If This Sounds Like You

If several signs apply, the response depends on where you are. If you haven't bought yet, the simplest fix is the most powerful: run the numbers at a lower price point and buy less house than the bank approved. The approval is a ceiling, not a target. Confirm a comfortable figure with the mortgage affordability calculator rather than the maximum the lender offers.

If you're already in the home, options include refinancing if rates have dropped meaningfully since you bought, aggressively eliminating other high-rate debt to free monthly cash flow and lower your DTI, adding an income source, or, in serious cases, speaking with a HUD-approved housing counselor about modification options. This is also a question the built-in AI assistant on the calculator pages handles well: tell it your income, payment, and other debts, and it can show whether you're inside the safe zone and which lever moves the needle most. A mortgage that's too expensive is a solvable problem, but only once you've named it honestly.

Frequently Asked Questions

What percentage of income should go to a mortgage payment?

The standard guideline is that your total housing costs, including principal, interest, property taxes, and insurance, should not exceed 28% of your gross monthly income. However, because your mortgage payment comes out of take-home pay rather than gross pay, a more accurate check is keeping housing below 35% of your actual net monthly income after taxes and deductions.

What is a debt-to-income ratio and what is a good DTI for a mortgage?

Your debt-to-income ratio (DTI) is the percentage of your gross monthly income consumed by all minimum debt payments combined, including your mortgage, car loans, student loans, and credit card minimums. Lenders typically approve mortgages up to a 43 to 50% DTI, but financial planners consistently recommend keeping total DTI at or below 36% to maintain meaningful financial flexibility and savings capacity.

What does it mean to be house poor?

Being house poor means your mortgage and housing costs consume so much of your monthly income that you have little or nothing left for savings, retirement contributions, emergencies, or ordinary life expenses. You are technically current on the mortgage but making no financial progress in other areas. The mortgage is being serviced, but the financial cost is a complete inability to build wealth or absorb unexpected expenses.

Is it bad to put less than 20% down on a home?

Putting less than 20% down is not automatically problematic, but it triggers private mortgage insurance (PMI), adding $100 to $300 per month to your payment with no benefit to you. It also means a larger loan balance, a higher monthly payment, and less equity cushion if values decline. The specific concern is when a minimum down payment is chosen because there simply wasn't enough saved, and the resulting payment is already a financial stretch.

What should I do if my mortgage is too expensive?

If you haven't bought yet, run the numbers at a lower price point before committing. If you're already in the home, options include refinancing to a lower rate if rates have fallen significantly since you originated your loan, eliminating other high-rate debt to improve total DTI and monthly cash flow, adding a supplemental income source, or contacting a HUD-approved housing counselor to explore modification or forbearance options if the situation is severe.