Coast FIRE: How Much to Save Now So You Can Stop Saving Forever

Coast FIRE is the amount you need invested today so compound growth alone funds your retirement, with no further contributions. Here is how to calculate your Coast FIRE number, with a worked example by age.

Imagine reaching a point where you never have to save another dollar for retirement, decades before you actually retire, and still ending up with a full nest egg. That's not a fantasy; it's a specific, calculable number called Coast FIRE, and it's one of the most freeing ideas in personal finance. Once your invested savings hit your Coast FIRE number, compound growth alone carries you to a comfortable retirement while you stop contributing entirely. Here's what Coast FIRE means, how it differs from regular FIRE, and exactly how to calculate your own number.

The traditional financial independence path asks you to save aggressively for decades. Coast FIRE flips the hardest part to the front: save intensely early, hit your number, then coast. After that, you only need to cover your current living expenses, freeing you to work less, switch to a job you love, or simply stop stressing about retirement. The magic that makes it possible is the same force behind all wealth: time.

What Coast FIRE Actually Means

Coast FIRE is the amount you need invested today so that, with zero further contributions, normal market growth will compound it into your full retirement target by the time you retire. You've front-loaded all the saving you'll ever need to do, and the market does the rest of the work for the remaining years.

The key distinction is that Coast FIRE doesn't mean you stop working; it means you stop saving for retirement. You still need income to cover today's rent, food, and life, but none of that income has to go toward retirement anymore. That single change, removing the retirement-savings burden from your monthly budget, is what gives Coast FIRE its sense of freedom. The pressure that drives most people's careers quietly lifts.

Coast FIRE vs Regular FIRE vs Barista FIRE

The FIRE world has several flavors, and confusing them leads to chasing the wrong number. Understanding where Coast FIRE sits makes its appeal clear.

- Regular FIRE: you've saved enough to live off your investments entirely and never work again. The full finish line, usually 25 times your annual spending.

- Coast FIRE: you've saved enough that you never need to contribute again, but you still work to cover current expenses while your investments grow untouched to the full FIRE number.

- Barista FIRE: a halfway point where part-time or lower-stress work covers your living costs, often for the benefits, while your investments grow.

Coast FIRE is the most achievable of the three for young people, because it depends on time more than on a huge balance. The earlier you reach it, the smaller the number needs to be, which is the opposite of how most people assume retirement works. It's the milestone you can realistically hit in your thirties, long before the others come into view.

How to Calculate Your Coast FIRE Number

The calculation has two steps. First, find your full FIRE number: your expected annual retirement spending times 25, based on the 4% rule. If you'll spend $50,000 a year in retirement, your FIRE number is $1.25 million.

Second, discount that target back to today using expected investment growth. The formula is your FIRE number divided by (1 + return rate) raised to the number of years until retirement. At a 7% return with 35 years to go, you divide $1.25 million by 1.07 to the 35th power, which is about 10.7, giving a Coast FIRE number near $117,000. Reach roughly $117,000 invested by 30 and, untouched, it grows to $1.25 million by 65. Run your own figures with the FIRE calculator and confirm the growth with the compound interest calculator.

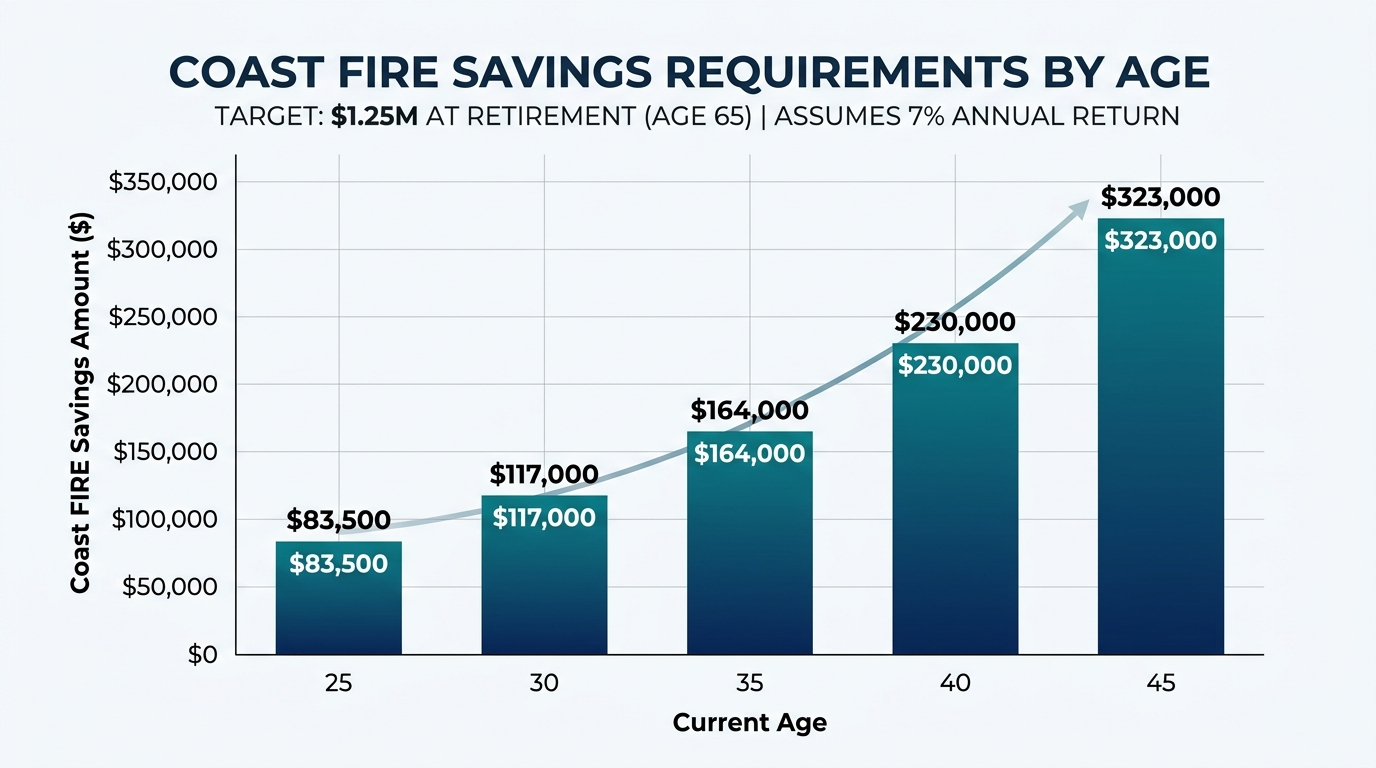

A Worked Example: Coast FIRE by Age

The number drops dramatically the earlier you hit it, because money has more time to compound. Here's the Coast FIRE number at different ages, all aiming for a $1.25 million target at 65, assuming a 7% annual return.

| Current age | Years to grow | Coast FIRE number |

|---|---|---|

| 25 | 40 | ~$83,500 |

| 30 | 35 | ~$117,000 |

| 35 | 30 | ~$164,000 |

| 40 | 25 | ~$230,000 |

| 45 | 20 | ~$323,000 |

The gap between the rows is the entire argument for starting early. A 25-year-old needs about $83,500 to coast; a 45-year-old needs nearly four times that for the identical retirement, because they've lost twenty years of compounding. Saving hard in your twenties isn't about deprivation; it's about buying your freedom decades cheaper than it will ever be again.

Why Hitting Coast FIRE Early Changes Everything

Reaching Coast FIRE doesn't make you rich overnight, but it changes your relationship with work in a profound way. The day your investments cross the line, the existential pressure of "am I saving enough for retirement" simply disappears, because the answer is permanently yes. Whatever happens next, retirement is handled.

That security opens real options. You can take the lower-paying job you actually enjoy, drop to part-time, start a business, take a career break, or move somewhere cheaper, all without sabotaging your future, because your retirement is already on autopilot. Coast FIRE converts decades of financial anxiety into decades of optionality. You're no longer working to fund retirement; you're only working to fund today, and today is far cheaper than today plus a retirement you haven't built yet.

What to Do After You Coast

Once you've hit your number, the strategy shifts from accumulation to simply not interfering. Leave the investments alone, keep them broadly diversified, and let compounding run. The one rule is to avoid touching the coast portfolio, because withdrawing from it breaks the math that makes the whole plan work.

Beyond that, you're free to optimize for life rather than for savings. Some people keep working and saving anyway, which pulls their full retirement earlier or richer. Others genuinely downshift. Check that your trajectory still holds with the retirement calculator every few years, since a market stretch below 7% or higher spending can move the target. As long as the portfolio is on track, the rest of your choices are yours to make.

Find Your Number

Coast FIRE turns a vague someday into a concrete, motivating target. Calculate your full FIRE number, discount it back to today at your expected return, and you have a single figure that, once reached, ends your retirement-saving obligation forever. For young earners especially, it's a far more achievable and energizing goal than the distant full-FIRE finish line.

This is a perfect question for the built-in AI assistant on the calculator pages. Tell it something like "I'm 30, want to retire at 65 on $50,000 a year, what's my Coast FIRE number and am I close," and it walks through the target and your gap instead of leaving you with a bare formula. Model how aggressively to invest now with the investment calculator. The earlier you reach your number, the cheaper your freedom, so the best day to start is today.

Frequently Asked Questions

What is Coast FIRE?

Coast FIRE is the point at which you have enough invested that, with no further contributions, normal market growth will compound it into your full retirement target by the time you retire. You still work to cover current expenses, but you no longer need to save for retirement.

How do I calculate my Coast FIRE number?

First find your full FIRE number by multiplying your expected annual retirement spending by 25. Then divide that by (1 plus your expected return) raised to the number of years until retirement. At 7% over 35 years, a $1.25 million target gives a Coast FIRE number of about $117,000.

What is the difference between Coast FIRE and regular FIRE?

Regular FIRE means you have saved enough to live off your investments and never work again. Coast FIRE means you have saved enough that you never need to contribute again, but you still work to cover current living costs while your investments grow untouched to the full FIRE number.

Does Coast FIRE mean I stop working?

No. Coast FIRE means you stop saving for retirement, not that you stop working. You still need income to cover your expenses today, but none of it has to go toward retirement, which frees you to work less, change careers, or take a lower-paying job you enjoy.

Why is the Coast FIRE number smaller if you start earlier?

Because money has more time to compound. A 25-year-old might need about $83,500 to coast to a $1.25 million retirement, while a 45-year-old needs around $323,000 for the same goal, since they have twenty fewer years of growth working for them.

What return rate should I use for Coast FIRE?

Many people use a 7% nominal return, the rough long-run average for a diversified stock portfolio. For a more conservative, inflation-adjusted estimate, some use 5%. A lower assumed return produces a higher, safer Coast FIRE number.

What happens after I reach Coast FIRE?

You leave the invested portfolio alone and let it compound, avoiding withdrawals so the math holds. You only need to earn enough to cover current expenses. Many people keep working and saving anyway, which pulls their full retirement earlier or makes it larger.