Annual vs Monthly Subscriptions: The Break-Even Math Nobody Runs

Paying annually promises a discount, but it only saves money if you keep the service past the break-even month. Here is how to calculate the real discount and decide annual or monthly for every subscription.

Every subscription service nudges you toward the annual plan with the same promise: "save 17%, get two months free." It sounds like an obvious win, so most people either take it without thinking or refuse it without thinking. Both are mistakes, because whether annual actually saves you money depends on a single break-even question almost nobody runs. Pay annually for something you quit in month three and you've lost money, not saved it. Here's the simple math behind annual versus monthly subscriptions, and the rule that tells you which to pick every time.

This is a tiny calculation with an outsized payoff, because the average household now juggles dozens of subscriptions. Getting the annual-versus-monthly choice right across all of them, and cancelling the ones that fail the test, can quietly recover hundreds of dollars a year. It starts with understanding what that "discount" really is.

The Discount Hiding in "Pay Annually"

The annual discount is real, and it exists for a reason that benefits the company more than you. When you pay for a year upfront, the business gets its cash immediately, locks you in for twelve months, and dramatically reduces the chance you'll cancel on a whim. In exchange, it shares a slice of that value with you as a discount, typically 15 to 20%.

A common structure is "two months free," meaning the annual price equals ten months of the monthly rate. A service at $15.99 a month costs $191.88 over a year monthly, but maybe $159.99 if you pay annually, saving about $32, or roughly 17%. The discount is genuine, but it's a bet by the company that you'll stay subscribed all year, whether you use the service or not. Whether the bet pays off for you depends entirely on whether you'd have kept it that long anyway.

How to Calculate the Real Annual Discount

Don't trust the marketing percentage; calculate it yourself, because the advertised number isn't always what it seems. The honest discount is the monthly price times twelve, minus the annual price, divided by the monthly-times-twelve total. That gives you the true percentage you save by prepaying.

Using the example: ($15.99 times 12, which is $191.88) minus $159.99 equals $31.89 saved, divided by $191.88 is about 17%. Run this for each subscription, because the real discount varies wildly: some annual plans save you 30%, others a measly 8%, and a few barely differ at all. The discount calculator does this in seconds, and the percentage calculator helps you compare offers side by side. A bigger discount makes annual more tempting, but it still has to clear the break-even test.

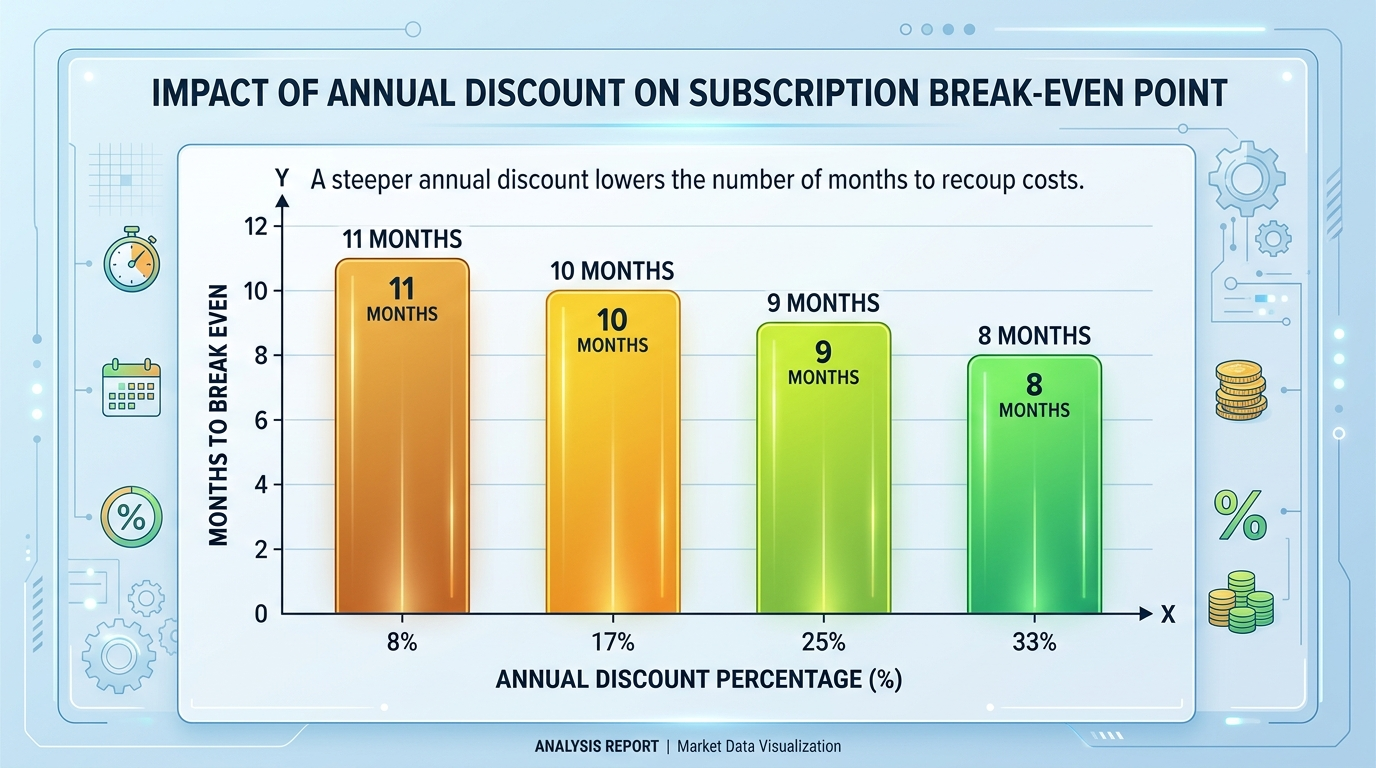

The Break-Even Question: Will You Still Use It?

Here's the part nobody runs. If an annual plan costs the equivalent of ten months of monthly payments, then annual only saves money if you keep the service longer than ten months. Cancel at month nine and you'd have paid less by going monthly. The break-even point is the number of monthly payments the annual plan equals.

| Annual plan equals... | Discount | Break-even: keep it at least |

|---|---|---|

| 11 months of monthly | ~8% | 11 months |

| 10 months of monthly | ~17% | 10 months |

| 9 months of monthly | ~25% | 9 months |

| 8 months of monthly | ~33% | 8 months |

The rule falls out cleanly: a bigger discount means a lower break-even, so deeper discounts are safer bets. The honest question to ask before clicking "pay annually" is simply, "Am I confident I'll still want this past the break-even month?" If yes, take the discount. If you're unsure, monthly is the cheaper hedge.

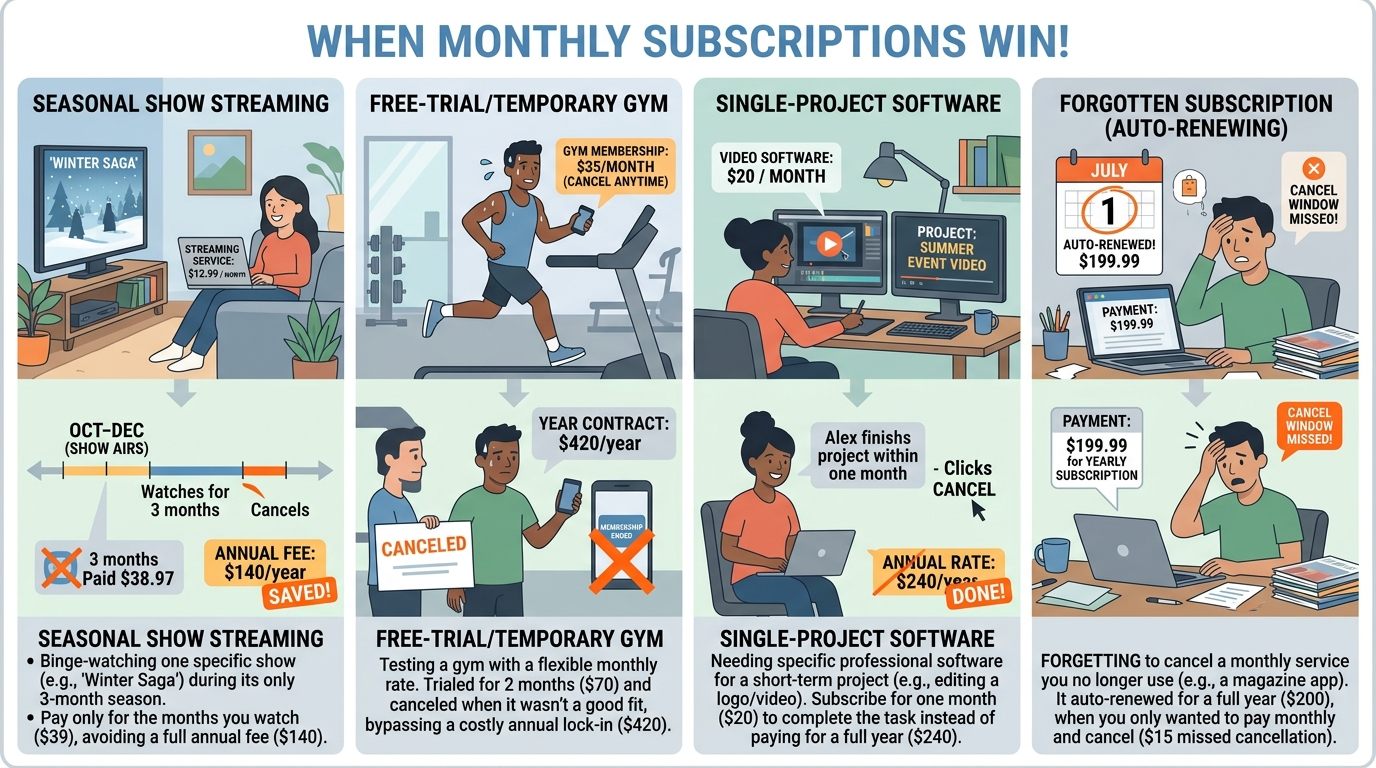

When Monthly Actually Wins

Monthly isn't just the default for the indecisive; it's genuinely the smarter choice in several situations. It wins whenever there's a real chance you'll cancel before the break-even month, which is more often than people admit.

Choose monthly for anything seasonal or short-term: a streaming service you want for one show, a gym membership you're "trying," software for a single project, or any subscription you've cancelled and resubscribed to before. Monthly is also right when you have a history of forgetting subscriptions, because an annual plan you forget renews for another full year before you notice, the opposite of saving. The flexibility of monthly has real value when your future use is uncertain, and that value often outweighs a modest discount.

The Opportunity Cost of Prepaying a Year

There's a smaller, subtler cost to paying annually: you hand over twelve months of cash today instead of spreading it out. That money could have stayed in your account, earning interest or simply staying available for emergencies, until each month came due.

For a single $160 subscription, this opportunity cost is tiny, a dollar or two, and not worth worrying about. But it scales. If you prepay annually on a dozen services at once, you might tie up over a thousand dollars upfront, and the timing matters more if money is tight. The compound interest calculator shows the effect is minor for small sums, so for most subscriptions the prepayment cost shouldn't sway you. The cancellation risk is the factor that actually decides it.

How to Take an Annual Plan Safely

If you do choose annual, a couple of small habits protect you from the one real downside: an unwanted auto-renewal a year later. The discount is worth taking when you're confident, as long as you don't let it quietly roll into a second year you didn't decide on.

First, set a calendar reminder for about eleven months out, a few weeks before the renewal date, so you make an active choice to continue rather than a passive one. Second, check whether you can turn off auto-renewal immediately after subscribing, which many services allow while still honoring your full paid year. That way the plan simply ends unless you deliberately renew it. These two minutes of setup turn an annual plan from a "set and forget" trap into a deliberate yearly decision, which is exactly what it should be. The savings are only real if the renewal stays your choice.

A Simple Rule for Every Subscription

Pull it together into one habit. Once a year, list every subscription you pay for, calculate the real annual discount on each, and ask the break-even question: will you confidently use it past the break-even month? Take annual on the high-confidence, high-discount services; keep monthly on the uncertain ones; and cancel anything you can't justify either way.

This audit is where the real money is, not in the annual-versus-monthly choice itself but in catching the subscriptions you forgot you had. This is a good task for the built-in AI assistant on the calculator pages: tell it "this service is $15.99 monthly or $159.99 annually, and I'm not sure I'll keep it past summer," and it runs the break-even and gives you a straight recommendation. Set a target for what you'd rather do with the savings using the savings goal calculator. The discount is only a discount if you would have stayed anyway, and now you'll always know which is which.

Frequently Asked Questions

Is it cheaper to pay for a subscription annually or monthly?

Annual is cheaper only if you keep the service past its break-even point. Most annual plans equal about ten months of the monthly price, so you save money only if you stay subscribed longer than ten months. Cancel earlier and monthly would have cost less.

How do I calculate the real discount on an annual plan?

Multiply the monthly price by twelve, subtract the annual price, then divide by the monthly-times-twelve total. For a $15.99 monthly plan versus a $159.99 annual plan, that is a saving of about $32, or roughly 17%.

What is the break-even point for an annual subscription?

It is the number of monthly payments the annual price equals. If the annual plan costs ten months of monthly payments, the break-even is ten months: keep the service longer than that and annual wins, cancel sooner and monthly would have been cheaper.

When is a monthly subscription the better choice?

Choose monthly for anything seasonal, short-term, or uncertain, such as a streaming service for one show, a gym you are trying out, or software for a single project. Monthly is also safer if you tend to forget subscriptions, since an annual plan can auto-renew for another full year.

Does paying annually have any downside besides commitment?

Yes, a small one: you pay twelve months of cash upfront instead of spreading it out, so that money cannot earn interest or stay available for emergencies. For a single subscription the cost is tiny, but it adds up if you prepay many services at once.

How much can I save by reviewing my subscriptions?

The biggest savings usually come not from the annual-versus-monthly choice but from cancelling subscriptions you forgot you had. People tend to underestimate their subscription spending significantly, so an annual audit often recovers hundreds of dollars a year.

How do I avoid an unwanted annual renewal?

Set a calendar reminder about eleven months after subscribing, a few weeks before renewal, so you make an active decision. Many services also let you turn off auto-renewal right after signing up while still honoring your full paid year.